With Treasury Bill Yields At 5%, Should The 60/40 Portfolio Now Be The 60/30/10 Portfolio?

Cash is no longer trash and investors should consider adjusting their portfolios to account for it.

It wasn’t that long ago that the 60/40 portfolio was declared dead. After a decades-long bull market in bonds that helped make the 60/40 portfolio one of the best investment strategies in the world, conditions changed when the Fed dropped the Fed Funds Rate to 0% during the financial crisis. That’s essentially the starting point for when investors began considering the “40” in the 60/40 portfolio to be dead money.

In reality, that wasn’t necessarily the case. Yes, the yields on Treasury bills, short-term CDs and money market accounts dropped to nearly nothing, but yields on long-term Treasuries continued to decline pretty much until the COVID pandemic in 2020. That provided investors with capital gains to offset the declining yields in this segment of the bond market and make long-term Treasuries still a viable part of a portfolio’s fixed income sleeve of a portfolio.

Where things really changed was in 2020. That’s when long-term Treasury yields dropped to below 1%. The gravy train for capital growth from bonds had effectively ended and with Treasuries earning next to nothing in terms of income, there was very little upside in fixed income. That’s really when the 60/40 portfolio became dead to many investors.

The “40” in 60/40 is NOT dead!

With bonds considered to be a non-starter with many investors, the search for alternatives got a little weird. Dividend equities were where a lot of folks ended up in their search for yield, but that, of course, raised the risk in portfolios. Some opted for real estate. Some indicated that they were pivoting towards covered call strategies. No matter what, investors largely opted for 100/0 portfolios. Those portfolios bottomed out in 2022 when both stocks and bonds entered bear markets at the same time.

The environment today, however, is different. The bear market in bonds last year was no doubt painful, but it also lifted yields off of their historically low levels to the point where they became a legitimate option for investors again. The most aggressive Fed rate hiking cycle in history has also managed to lift the yield on 3-month Treasury bills to more than 5.5%, the highest they’ve been since late 2000.

Other major bond ETFs are also paying similarly juicy yields. The iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) is at 5.65%. If you want to stay on the safer end, the iShares AAA-A Rated Corporate Bond ETF (QLTA) is at 5.36%. On the riskier end, the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) is at 8.11%. Regardless of whether you want short-term or long-term, government or corporate, investment-grade or high yield, bonds are back (at least in terms of being a legitimate complement to equities again)!

Treasury ETF Yield Options: Take The 5% And Run?

The big question is how you reposition a portfolio, which could have consisted of as much as 90-100% equities in recent years back to a more balanced 60/40 mix? There are a couple of considerations (outside of the standard “this decision should be made based on your personal risk tolerance, objective, time frame, etc.” disclaimer).

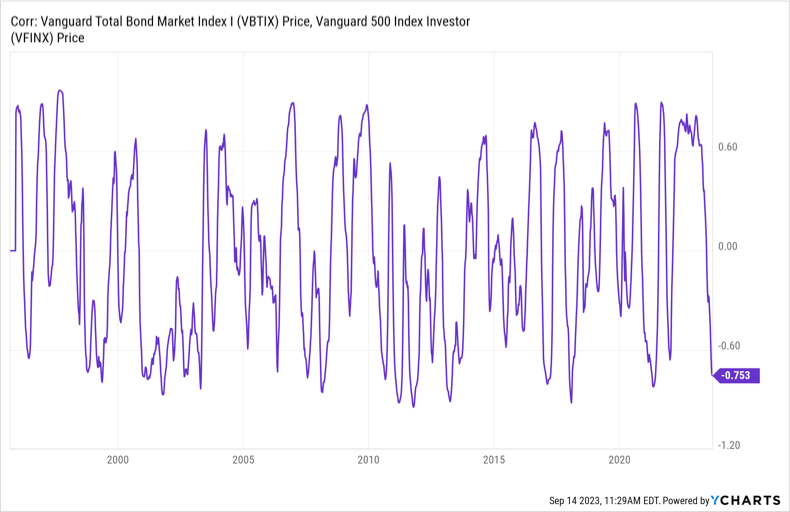

First, bonds are often considered a risk counter-asset to equities. When one zigs, the other zags. In reality, the results are pretty mixed. Bonds usually swing back and forth between a positive & negative correlation to equities pretty regularly. That makes them a good, not great, diversifier.

People will look at 2022 and say that there was clearly no diversification benefit when both stocks and bonds were falling together. That’s true, but remember that last year was the extreme outlier. The fact that inflation was above 8% at the time throws a lot of what we traditionally expect from the markets out the window. Inflation isn’t expected to get back to a sustainable 2% level until 2025, so the short-term might still be a little wonky for a while, but long-term relationships should resume.

The second consideration is whether you’re interested simply in yield or yield/capital gains. If you’re interested in yield, I see no reason to look beyond something like the SPDR Bloomberg 1-3 Month T-Bill ETF (BIL) or the iShares Treasury Floating Rate Bond ETF (TFLO). Both of these are paying right around 5.3% and come with almost no volatility. In terms of pure yield, I think these are some of the best plays right now.

The only reasons I see for venturing further out on the maturity spectrum are 1) you want to lock in current rates for long (this would be for buying individual bonds since bond ETF yields fluctuate with conditions) or 2) you’re betting on a move in rates.

The most likely bet right now is probably on a recession coming in the next 3-6 months on long-term Treasury bond yields falling significantly. The iShares 20+ Year Treasury Bond ETF (TLT) has a duration of roughly 17 years (which means for every 1% move in interest rates, TLT could move around 17%). That could end up being some big upside were a flight to safety trade to occur.

60/40 vs. 60/30/10

I wouldn’t normally say that investors should substitute cash for part of their fixed income portfolio, especially since cash will very likely lag fixed income & equities over the long-term. Right now, however, is an unusual situation. Nearly risk-free 5% yields from Treasury bills are available for the taking and I think investors should take advantage. This opportunity hasn’t arisen in decades and could disappear quickly should recessionary risks rise or the Fed begins cutting rates again.

Either BIL or TFLO make great options in this scenario. I think the 60% equity allocation should probably remain as is, but with the current yield environment and the fact that I think credit risk is grossly underpriced right now, the risk/reward comparison between longer-term fixed income and cash tilts heavily in the latter’s favor.