Weekly Market Prep - 9/25/2023

Investors will watch equities for an extension of last week's declines, but the real action is still in the bond market.

Hope everyone had a great weekend & welcome back to ETF Focus!

It’s Monday, so let’s get back to the grind and ready for the week ahead!

Weekly Market Reset

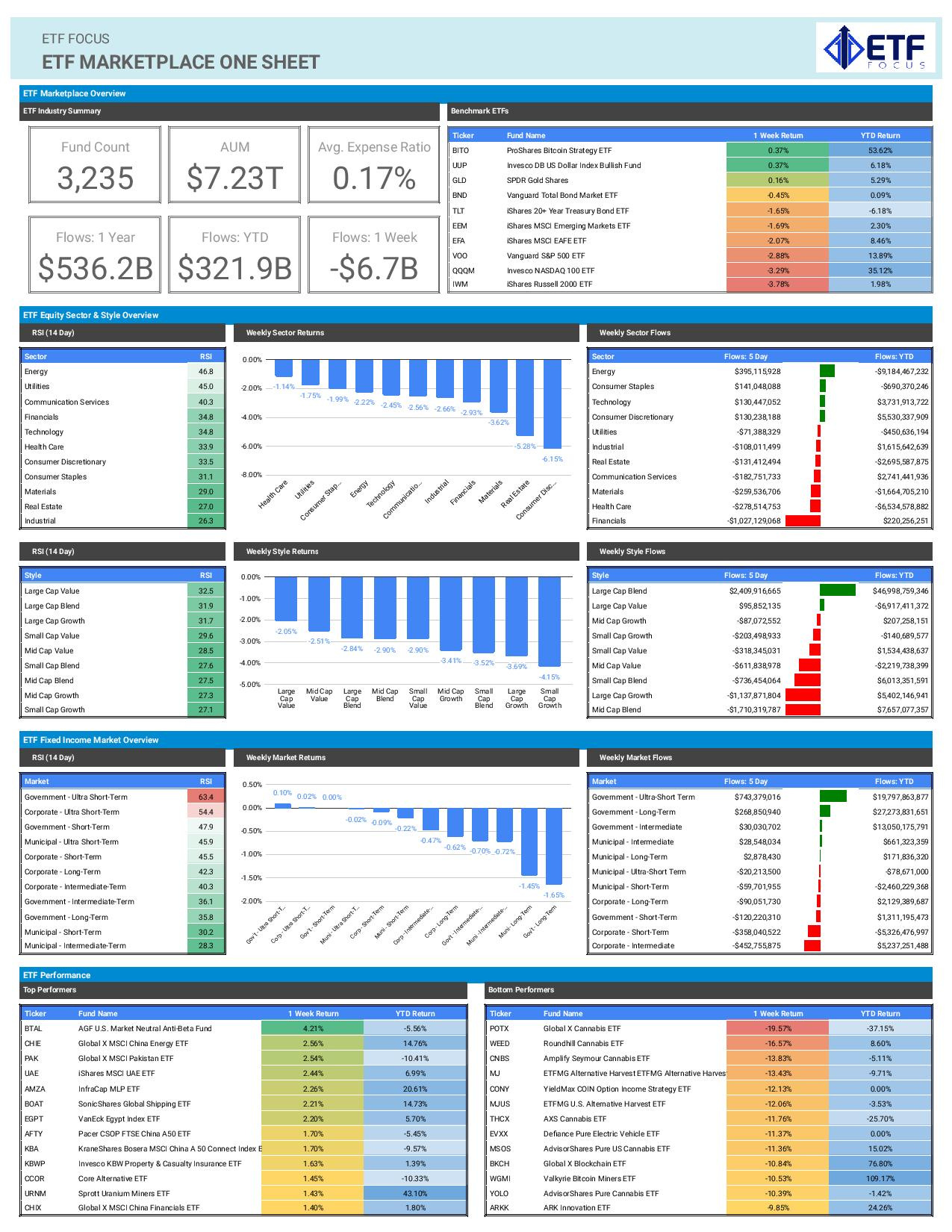

While last week’s significant declines in global equities were more headline grabbing, the action in the bond market is what investors should be most concerned about right now. The fact that long-term Treasury yields have been soaring over the past few months and the rise is only continuing to accelerate suggests that a major correction could be near. Real yields are getting to the point now where inflation expectations and the level of monetary constriction by the Fed are becoming noticeably imbalanced. The fact that the central bank is still indicating the potential for more rate hikes even as consumer credit levels look unsustainable and bankruptcies become more pervasive means that the markets will react accordingly to the conditions the Fed is setting. I believe that the sell-off in equities suggests investors may not be as confident in the soft landing narrative as they are, nor should they be.

If you look at history, sharp spikes in real yields, such as the one we’ve seen already in 2023, tend to be followed up with sharp drops off of a cliff. If inflation remains at roughly the same level that it’s at today, that means Treasury yields have to drop significantly if they’re going to copy history again here. The Fed tends to almost always be reactive, so it’s reasonable to think that the first potential rate cut won’t come until well into the 2nd half of 2024. That means the real potential for investors comes on the long end of the curve. Whether the entry point is soon or several months from now, I’m not sure, but I think that’s the direction we’re headed in - a larger risk-off sentiment shift that drags most risk assets down.

We should also be keeping a close eye on high yield spreads here. They’ve started moving higher again over the past several days and, while they’re still not even back to August levels yet, the sharp move higher after weeks of calm could be a warning sign considering what else is going on in stocks and bonds. The BofA high yield spread is at 3.93% as I write this. If it gets above 4% and holds that level, I don’t think there’s much standing in the way of it moving to 4.5%. If we get a move higher in nominal fixed income yields along with an expansion of spreads at the same time, that could mean a big negative move for junk bonds ahead. Spreads are the one thing that have been stubbornly resistant to price in market risks. If those start to give in, I think we’ve got a pretty consensus signal that conditions could turn very negative.

Key Economic Reports This Week

United States Durable Goods Orders (Wednesday)

United States Q2 GDP Final Reading (Thursday)

Spain preliminary September Inflation (Thursday)

Eurozone, France, Italy preliminary September Inflation (Friday)

United States Core PCE - August (Friday)

United States Personal Spending - August (Friday)

United States Personal Income - August (Friday)

Market Outlook

I think it’s going to be all about bond market yields again. With the major central bank announcements finally out of the way, the markets likely turn their focus to economic conditions again. In the United States, Friday’s economic calendar will likely make the end of the week more volatile since that could shape the market’s outlook for the Fed. I don’t think we’ll get anything that we don’t already know, but any significant deviations from expectations could get a reaction.

Utilities have been on a tear relative to the S&P 500 and we’re starting to see more defensive strategies participating in the risk-off pivot. This current rise in interest rates could lead to a final blow-off soon that ultimately ushers in the safe haven rally in Treasuries that has eluded the market for several quarters.