Weekly Market Prep - 4/22/2024

Market sentiment is sharply negative, but the magnificent 7, once again, have the opportunity to save the day.

Welcome back to ETF Focus!

It’s Sunday! That means it’s time to get prepped and ready for the week ahead!

What We’re Talking About This Week!

+ Weekly Market Reset

+ Key Economic Reports This Week

+ Dividend Landscape

+ Market Outlook

Weekly Market Reset

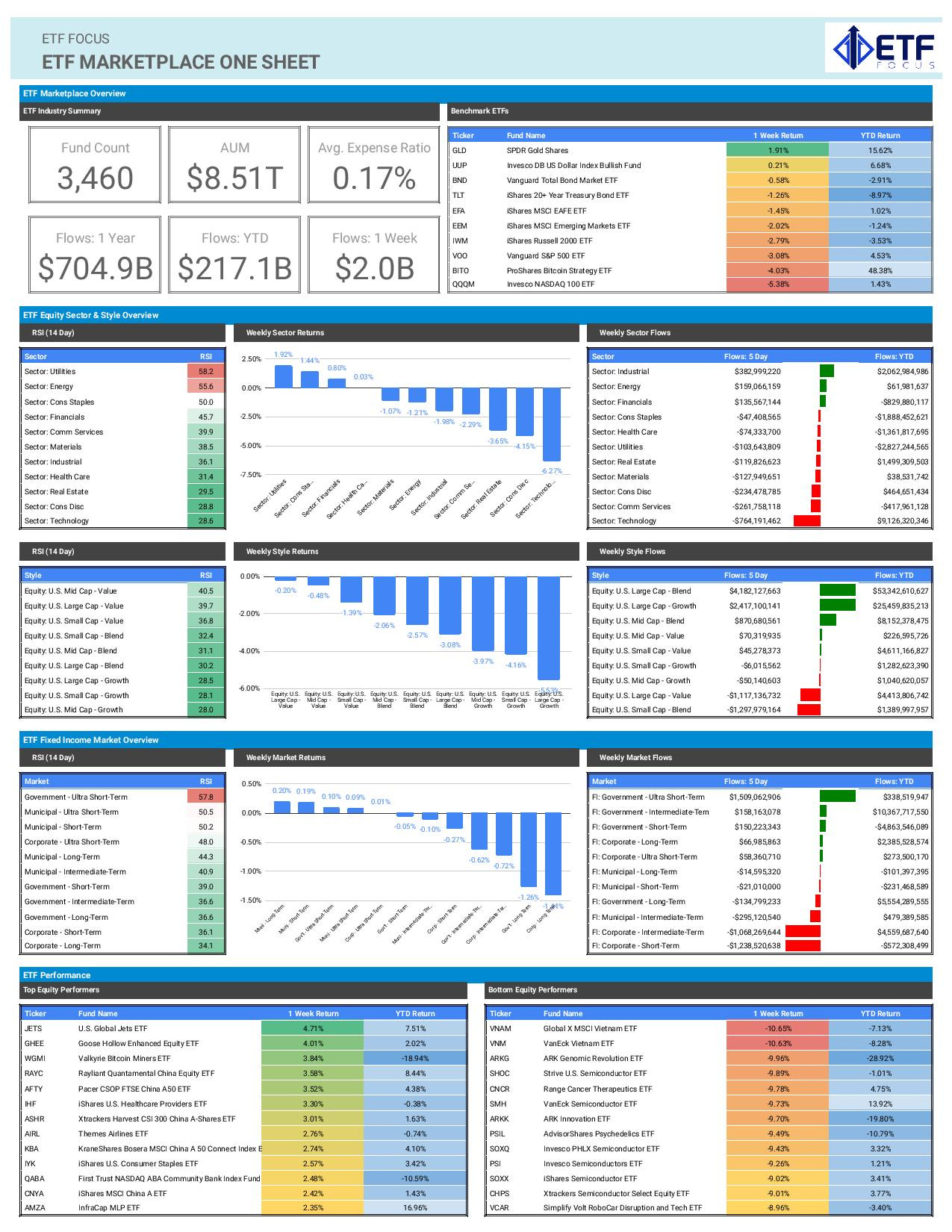

Even though the S&P 500 has been on the decline for three straight weeks, last week looked different than the others. After some ping-pong between growth and cyclicals, defensive sectors and strategies finally took over in major way! Utilities outperformed the S&P 500 by nearly 5%, while consumer staples lapped it by more than 4%. Value, low volatility and dividend stocks significantly outperformed their growth & high beta counterparts in a way that we really haven’t seen in months. Add this to the huge rally in gold and strength in the dollar and I think we have a very risk-off looking market right now. I don’t want to overweight a single week’s performance because we have seen these kinds of short-term blips before, but this is about as bearish a one-week signal as we’ve seen in some time.

The narrative backdrops all point to significant challenges ahead. While GDP growth and the labor market still look healthy (and could prevent the major averages from drawing down too far here), inflation is unquestionably headed in the wrong direction and Powell has finally acknowledged out loud that rate cuts are probably off the table for the time being. Although I’m not sure he’ll say it right now, I believe the Fed is in a neutral stance right now as opposed to the publicly stated dovish stance. Since Powell said that progress on inflation has stalled, I think the Fed will now be looking for a meaningful resumption of the disinflationary trend. I don’t think they can view what’s happened over the past 2-3 months as purely a speed bump in an otherwise downward trend. At best, I think the disinflationary trend has ended. At worse, I think we’re at least in a temporary re-inflationary cycle with an uncertain endpoint. That makes me believe that there’s potentially more downside ahead for risk assets.

If we look at investor net flow activity, we can see that confidence is definitely getting shaken here. Tech ETFs have seen the biggest inflows throughout much of 2024, but now they’re starting to see some of the biggest outflows. On the fixed income side, we saw a huge pickup in Treasury bill ETF inflows after a year of mostly modest activity. Short- and intermediate-term Treasury ETFs were also the next two categories with the biggest inflows. I won’t say that we’re seeing a flight to safety trade developing just yet in Treasuries because yields are mostly still trending higher, but the fact that investors are starting to pile back into these groups is a sign that they’re seeking safety right now.

And don’t sleep on emerging markets right now. I know they’ve been beaten down for….well, forever, but we’re potentially looking at a very early stage turnaround. If we use 2022 as a guide, value stocks and small-caps did well relative to the S&P 500 and I think that’s a function of investors shunning expensive growth stocks. We’re starting to see some of that behavior again, especially in the fact that small-caps aren’t really underperforming here despite the overall market correction. Emerging markets are filled with deep value companies and I don’t think it’s out of the question that investors reconsider this group if value stocks have another good run here. India is looking strong. Several economies are likely to be entering rate cutting cycles soon. Even China is showing some signs that its situation is beginning to improve.

Key Economic Reports This Week

Most people will be focused on the first Q1 GDP reading and it’s expected to be another good one. The one thing that’s been consistent throughout the past year or longer has been the resilient economy theme. Even higher interest rates and tighter financial conditions haven’t been able to slow it down thus far and it’s likely been unable to do so in Q1 as well. This should support any argument that the market bulls will try to make, but I think this expectation is largely baked in at this point.

The more interesting U.S. economic data, in my opinion, will be personal income & spending. We keep hearing about how the consumer is weakening, but spending and retail sales just haven’t supported that to this point. The one thing that may be changing is the labor market backdrop. The unemployment rate has ticked higher from its cycle low and the number of layoff announcements has been picking up. Perhaps that starts spilling over into spending figures soon, but I don’t think this will be the month.

Of course, we have to pay attention to the Bank of Japan meeting this week. It’s highly unlikely we’ll see any policy shifts here, but any signals on future direction will be what the market wants to hear. We’ve gone from the expectation for a slow but steady tightening of conditions at the beginning of the year to a high likelihood of no additional tightening for the foreseeable future. Inflation looks sustainable for the time being and that was the one thing that the decision to raise interest rates recently was predicated on. I’m not sure even that is a sure thing any more. I want to hear if the Japanese government is planning on intervening to save the yen because that could have global implications. The yen/dollar exchange rate is well past the level that’s triggered past interventions and we know that they’re watching it closely. I still think an intervention is inevitable and perhaps this is the week.

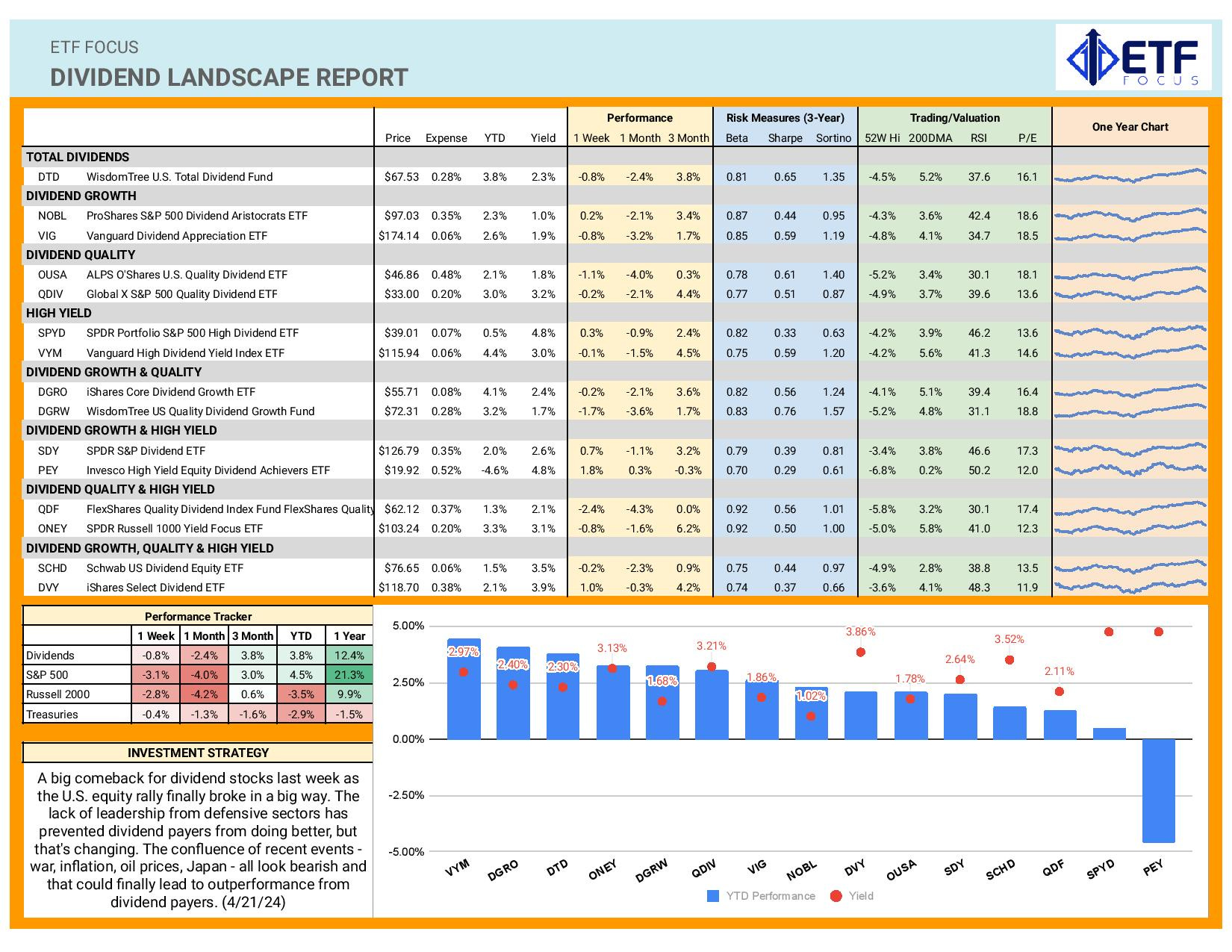

Dividend Landscape

Dividend stocks, along with other defensive strategies, finally had a big week of outperformance. Like I noted above, I don’t want to get overly excited by a single week because we’ve seen this kind of thing before, but it feels like sentiment may have genuinely changed over the past couple of weeks. Tech looks like it’s really fallen out of favor here and that could carry forward into this week. NVIDIA has been a market favorite over the past year and to see it drop 13% last week may have really put a crack in investor confidence. Apple, Microsoft and Facebook are all reporting this week. If they signal disappointing guidance like Netflix did, it could be another big down week for the market, although good (relatively speaking) for dividend stocks.

Market Outlook

At this point, market sentiment is quite poor and we’ll need to see some type of catalyst to turn it around. I actually think tech earnings could be it. The magnificent 7 stocks have demonstrated a lot of resilience when it comes to earnings and revenues over the past several quarters and they tend to deliver good guidance as well. If the sector can get that out of the big three companies reporting this week, we could see a reversal where tech/growth lead again while defensives turn into laggards for at least another week. I have middling confidence in this and think it really could go either way.

I see TIPS continuing to trend higher relative to Treasuries in general. The data certainly points to another uptick in inflation and TIPS have responded accordingly. Since the higher inflation trend, in my opinion, isn’t going away anytime soon, I think TIPS could continue a low, slow uptrend that’s been starting to build for a few weeks.

Overall, I’m retaining a cautious approach. The markets appear genuinely shaken here. High yield spreads and the VIX are both starting to move higher and those are usually strong signs that confidence is weak.

Looking better for: gold, low volatility, small-caps, TIPS

Looking worse for: Treasuries, emerging markets, healthcare