Weekly Market Prep - 4/15/2024

Portfolio positioning should be conservative with so many negative-tilting wild cards looming over the markets.

Welcome back to ETF Focus!

It’s Sunday! That means it’s time to get prepped and ready for the week ahead!

What We’re Talking About This Week!

+ Weekly Market Reset

+ Key Economic Reports This Week

+ Dividend Landscape

+ Market Outlook

Weekly Market Reset

Both stocks and bonds got smacked again last week with precious metals and dollar, once more, pushing higher. The old boogeyman, inflation, was largely to blame, but it was far from the only factor driving investors away from risk assets. The situation between Israel and Iran escalated quickly and threatens to create a cascade effect that could spill over into equities and oil prices. On top of that, the Bank of Japan still lies in the weeds threatening to intervene on the yen and send U.S. Treasury yields much higher in the process. The VIX moved to its highest level since October of last year, but in the teens it’s not yet indicating that investors are overreacting or panicking.

If investors aren’t yet concerned about the trend in inflation, they should be. Both the headline and core rates may be under 4%, but core inflation, in particular, has been trending higher for 9 months on a month-over-month basis. On a short-term annualized basis, it’s still running at more than 4% and isn’t showing signs of slowing down. If you look at the overall lay of the land - inflation trending over 4%, the unemployment rate under 4% and GDP growth at 3% - there’s no reasonable case to be made that the Fed should even be considering rate cuts at this point. The markets may finally be coming to terms with this and that’s contributing to some of the recent downward pressure on stock prices. I think if we get past the July Fed meeting without a rate cut, the next realistic possibility for one might be December if the central bank wants to avoid the lead-up to the presidential election.

I think it’s safe to say that the markets watched the Israel-Iran situation with only modest interest until word came on Thursday that an Iranian missile attack was imminent. The market reaction was interesting because for the first time in a while, we saw investors react with genuine risk-off behavior. Stocks fell and Treasuries rallied proving that the safe haven trade still exists and there is still some potential for long bonds here should political unrest escalate and oil prices spike. I expect that the rhetoric from all major parties involved this week will be bitter and pointed, but there’s ultimately more to be gained by both sides making their points and then de-escalating again. If that were to occur over the next several days, I think we could see a rebound in risk asset prices in relief. It’s all still very much in the air though.

The potential intervention of the yen by the Bank of Japan is getting a little lost in the shuffle here, but it could have a big impact on the forex market and long-dated Treasuries. If the BoJ decides to buy up yen to defend its value, its trillion-plus dollar position in Treasuries would be an obvious spot for it to draw from. The yen is still hovering above 153 and I believe that an intervention is still imminent.

Key Economic Reports This Week

The calendar will be relatively light in the United States with retail sales and building permits the only major reports dropping this week. Inflation, however, will take center stage again with the latest numbers coming from Canada, the United Kingdom and Japan. The U.K. report may be the most interesting of the three because the Bank of England appears more than ready to cut rates with the economy entering a technical recession in Q4. Inflation has been trending in the right direction and if it gets another reading that’s on target, the BoE may just say “close enough” and signal its first rate cut.

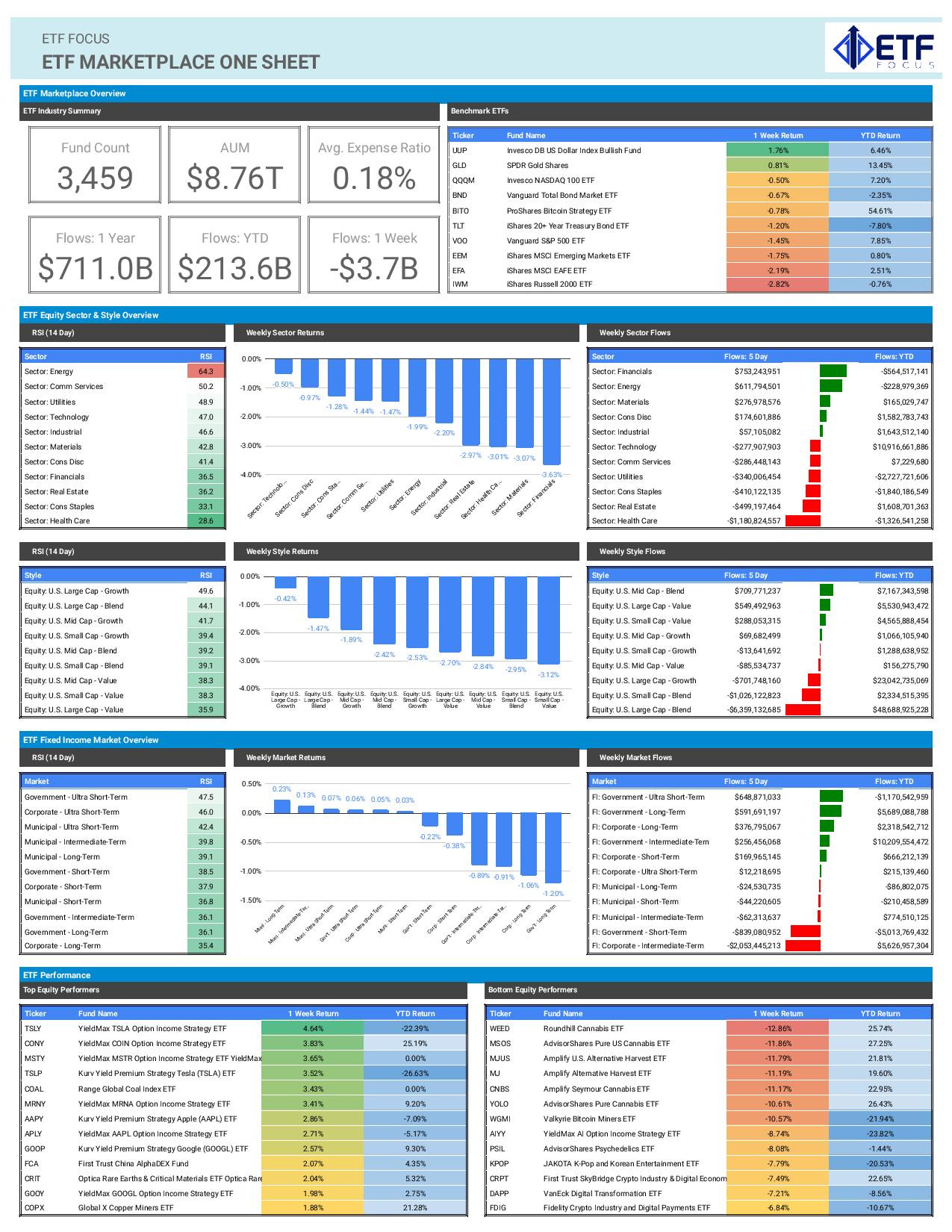

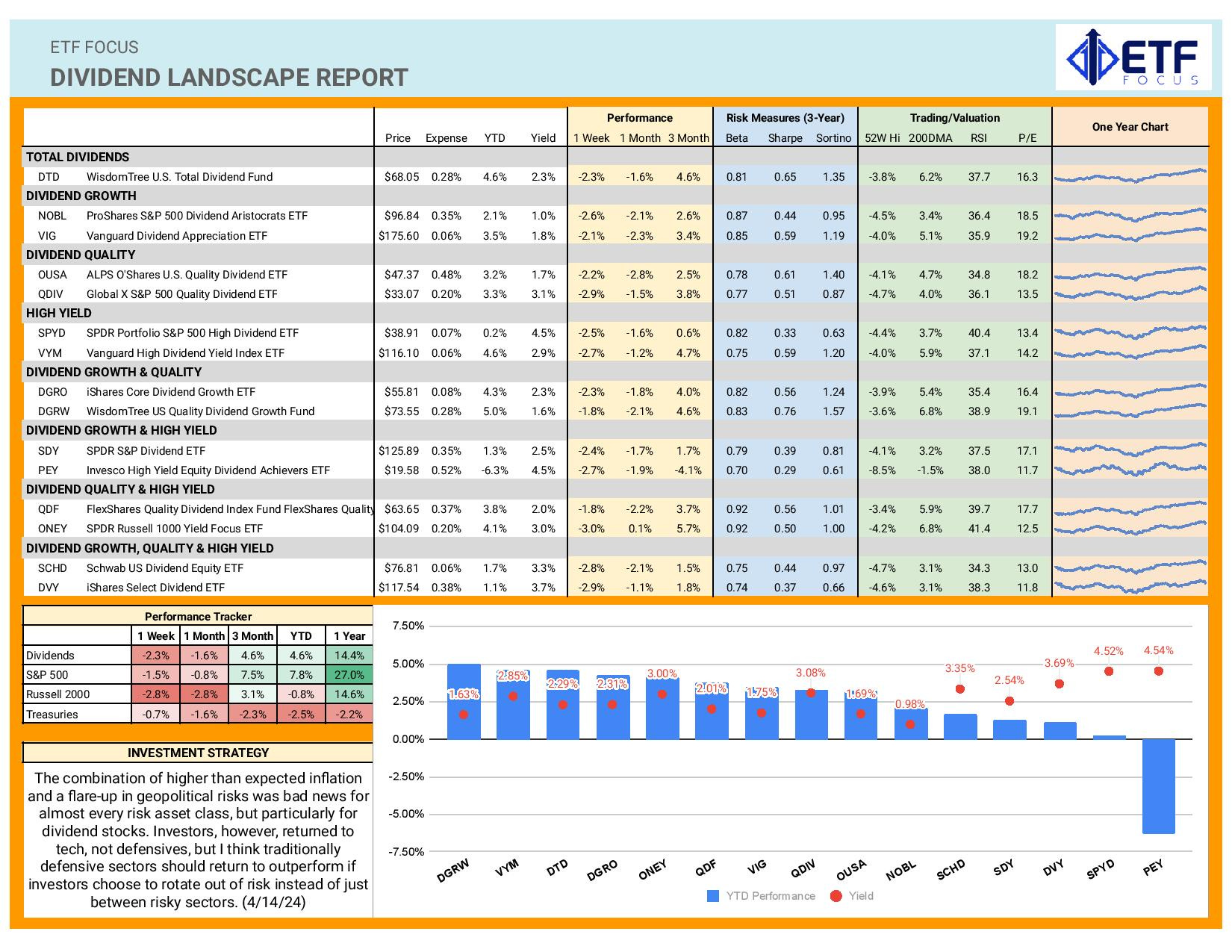

Dividend Landscape

Even though investors have been selling stocks over the past two weeks, they haven’t been rotating into defensive sectors. In 2022, rising inflation helped fuel massive outperformance from dividend payers, but we haven’t seen a similar trend this time around. The biggest difference this time around is that the economy overall looks fairly strong, which wasn’t the case two years, and that’s kept investors still testing the waters on cyclicals and growth stocks.

There are still plenty of potentially negative catalysts out there that can trigger more of a full-blown risk-off move. A delayed Fed rate cutting cycle and rising inflation have had their moments, but we have yet to see the big volatility spike that would usher in the return of safe haven trades. It feels like dividend stocks will struggle to maintain consistent leadership until something breaks.

Market Outlook

I think we’re in for another cautious week. Until we get some clarity on the geopolitical front and what the Bank of Japan plans on doing with respect to the yen, I don’t think the impetus exists for investors to feel comfortable bidding up stocks. With so many unknowns hanging over the markets, I feel like we’ll be in this gray area where there’s more downside than upside.

The dollar and gold seem like the only trades where there’s at least some degree of confidence that they’ll be on the rise again. Stocks look nervous. Bond yields seem to want to move higher rather than lower. I’d be keeping risk positioning on the conservative side until further notice.

Looking good for: dollar, gold, quality

Looking worse for: small-caps, financials, dividend stocks