Weekly Market Prep - 3/18/2024

Central banks take center stage this week, but it might be the Bank of Japan, not the Fed, that is most consequential.

Welcome back to ETF Focus!

It’s Sunday! That means it’s time to get prepped and ready for the week ahead!

What We’re Talking About This Week!

Weekly Market Reset

Inflation data was the main driver of market returns this week, but its interpretation of the numbers changed as the week went on. CPI in the U.S. came in hotter than expected, but traders seemed to take it in stride and send the major averages higher. Yet when the PPI number was released on Thursday, the markets seem to acknowledge that there could be a longer-term problem here.

Investors seemed to be taking the general stance that modestly higher inflation is OK as long as GDP growth remains healthy to support it. Now, I think we’re seeing that inflation is indeed re-accelerating and that’s going to prevent the Fed from making any major changes to interest rates this year. After two weeks of steadily falling long-term yields, the 10-year is back retesting the February high and could hit the highest level since November sometime this week. TIPS are outperforming long-term Treasuries here, but they remain on par with intermediate-term notes, so we’re not seeing a major influx of money going into inflation protection strategies yet. The curiosity around what the Fed will say in its quarterly projections will likely kick up volatility in the bond market this week.

We still have yet to see any real evidence of a flight to safety trade building in equities. Even though large-caps outperformed last week, it’s interesting that the best relative strength belongs to value stocks. A big reason for that is the recovery in cyclicals, but it’s also demonstrates that tech & growth are indeed falling out of favor. The “magnificent 7” have spent the past month and a half moving sideways relative to both the S&P 500 and the broader tech sector. Valuations are clearly being deflated a bit here, but that’s a trend that could continue if the Fed takes a more hawkish tone in its quarterly outlook this week. The futures market is still pricing in three rate cuts by the end of this year, but I would take the under on that at this moment. I suspect market expectations will shift hawkish post-Fed meeting this week.

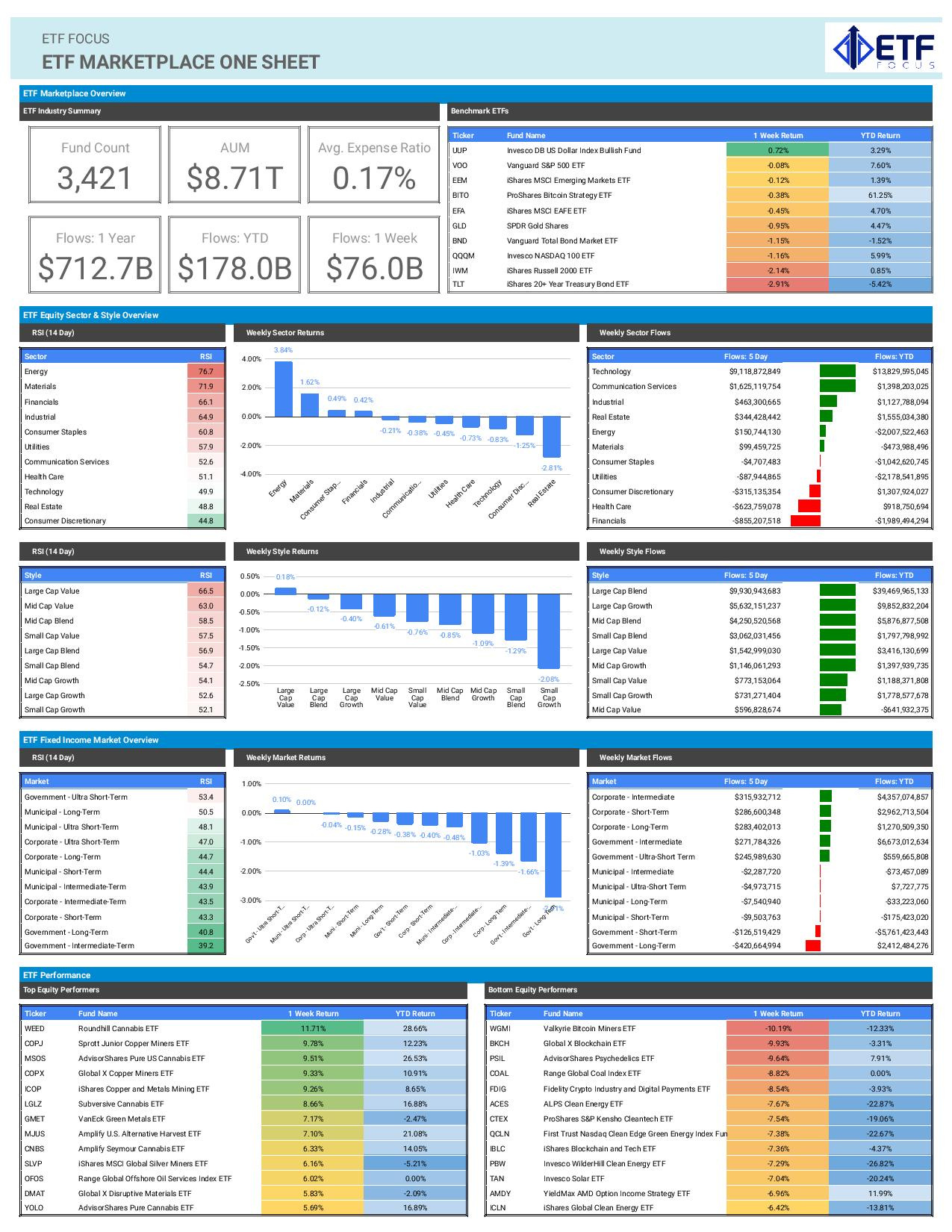

For the ETF market, in general, we saw another $76 billion of net inflows last week, putting us on pace for roughly $840 billion for the year. Anybody who tells you that this market is slowing down isn’t paying attention! Of course, bitcoin ETFs deserve some credit for this. The iShares Bitcoin ETF (IBIT) has seen the 3rd largest inflow year-to-date at more than $12 billion (the Fidelity Bitcoin ETF (FBTC) is #6 as well) behind only the Vanguard S&P 500 ETF (VOO) and the iShares Core S&P 500 ETF (IVV). Can IBIT get to #1 by the end of the year? Very unlikely since VOO and IVV have a big advantage and they tend to draw steady flows throughout the year, but the fact that we can even ask that question right now shows how popular the spot bitcoin ETFs have been.

Key Economic Reports This Week

It’s all about the central banks this week kicking off right away with the Bank of Japan on Monday night. Australia’s central bank also sets policy on Monday, we’ll get the Fed on Wednesday and the Bank of England on Thursday. The most important will be the BoJ, which is expected to finally end negative interest policy. The Fed will almost certainly hold steady, but its outlook for the rest of the year is what the street will be watching.

Inflation rates in Canada and the United Kingdom are expected to show a continuation of the global disinflationary trend.

Dividend Landscape

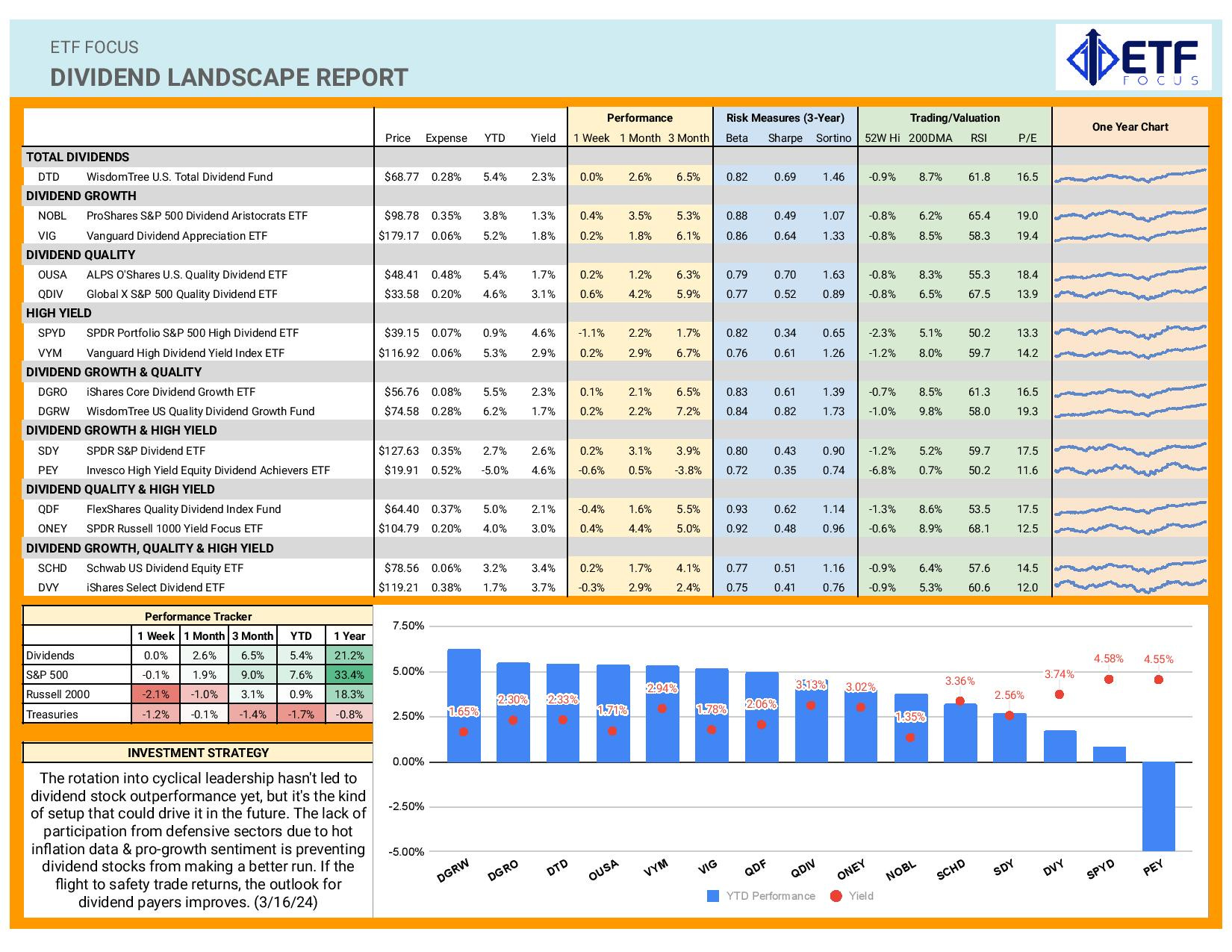

Dividend stocks are still struggling to kick it into gear even as the tech trade weakens. The advances made recently by cyclicals have been helpful, but traditional contributors, such as consumer staples and healthcare, have struggled to keep up with the market averages for a while now. Even as inflation shows signs of picking up again and the Fed is likely to push back its calendar on rate cuts this week, the markets largely seemed satisfied with overall conditions as long as growth continues. That’s going to give defensive issues precious little room to carve out a niche here and may keep dividend stocks on the back burner for now. None of the major dividend ETFs is beating the S&P 500 year-to-date, but the WisdomTree U.S. Quality Dividend Growth ETF (DGRW) has come the closest.

Market Outlook

As I mentioned above, it’s all about the central banks this week. The BoJ’s likely decision to bring its benchmark interest rate back up to 0% may be a “sell the news” event and could briefly stop the bleeding in Japanese equities that we’ve seen for a couple weeks. An unexpectedly hawkish message from the Fed mid-week could add some volatility and downside potential to U.S. equities this week, but investors have largely shaken off those messages following recent meetings. Investors could interpret it as a confirmation of what we think we already knew and use it as an excuse to try to push the S&P 500 and Nasdaq 100 higher again.

Bonds are likely in the trickiest spot here. I think there’s more pressure for long-term rates to move a bit higher and the Fed messaging will likely be the catalyst. I’ll be interested in seeing how gold responds. It’s leveled off over the past week, moving lower as rates moved higher, and we could see that again this week.