Vanguard's Achilles Heel

The popular ultra-low cost ETF market heavyweight actually has some vulnerabilities that could impact investors.

I’m probably not telling you anything you don’t already know when I say Vanguard is one of the biggest and best ETF issuers in the world. Its ultra-low cost approach to fund management fees has proven incredibly popular with investors, which makes it the go-to provider for investors simply looking to capture broad market exposure at minimal cost.

That doesn’t make Vanguard invincible though. Its reputation as the premier ultra-cheap index fund issuer comes with some drawbacks and challenges, both for investors and the company itself. That’s not to suggest that investors should abandon Vanguard or go searching for another broker to work with, but in some cases, depending on what you’re looking for in your portfolio, you may need to look elsewhere.

Where Is Vanguard Vulnerable?

Vanguard is clearly a market leader in the broad low-cost ETF market. That means the company could literally put the whole operation on autopilot and probably still rake in billions of dollars of fresh investor money. We’ve seen other fund issuers attempt to challenge Vanguard on cost and largely fail.

The SoFi Select 500 ETF (SFY) has waived its fee completely and charged 0.00% since its inception in April 2019. Right now, it’s sitting at just over $500 million in assets, a respectable number that will keep the ETF in business, but definitely not a blockbuster success. The SoFi Next 500 ETF (SFYX), which effectively measures the mid-cap market, also has a 0.00% expense ratio. It has just $60 million in assets.

Salt Financial even tried launching a negative expense ratio ETF around the same time that the SoFi ETFs debuted. Its -0.05% fee meant that the company would actually pay you to invest in the Salt Low truBeta U.S. Market ETF (LSLT) up to a certain asset level. The fund, however, never got much above $10 million in assets. In June 2020, Pacer announced that it was acquiring LSLT and immediately raised the expense ratio to 0.60%, effectively negating its one big selling point. In February 2022, Pacer shuttered the ETF altogether.

The takeaway from this is that Vanguard essentially has the low cost ETF marketplace cornered. Investors really don’t care if there’s a cheaper product out there. They want to invest in Vanguard ETFs almost regardless of the cost and will continue using the company as its all-in-one investing shop.

But there’s one area of the ETF marketplace that Vanguard has had trouble breaking into. Basically anything else!

Struggling Outside Of Plain Beta ETFs

If you look up and down the Vanguard ETF lineup, it consists almost entirely of broad index-based ETFs. There are no real frills or surprises in that approach, but it also leaves a pretty sizable hole in the areas that investors continue to show an increased interest in. Namely, country, factor, thematic and commodities ETFs.

It hasn’t been for a lack of trying though. Vanguard actually has ventured outside of its core competency of index funds into actively-managed ones, but with very limited success. Over its history, Vanguard has launched a total of 7 actively-managed ETFs.

The largest and most successful of the bunch has been the Vanguard Ultra-Short Bond ETF (VUSB) with more than $4 billion in assets since its launch roughly two and a half years ago. The fact that it’s done the best of the bunch is probably because it looks the least like an outsider. It fits seamlessly into the rest of the Vanguard fixed income lineup and most investors probably don’t even realize that it’s actively-managed. Its 0.10% expense ratio is also consistent with the ultra-low fees we see with other Vanguard ETFs.

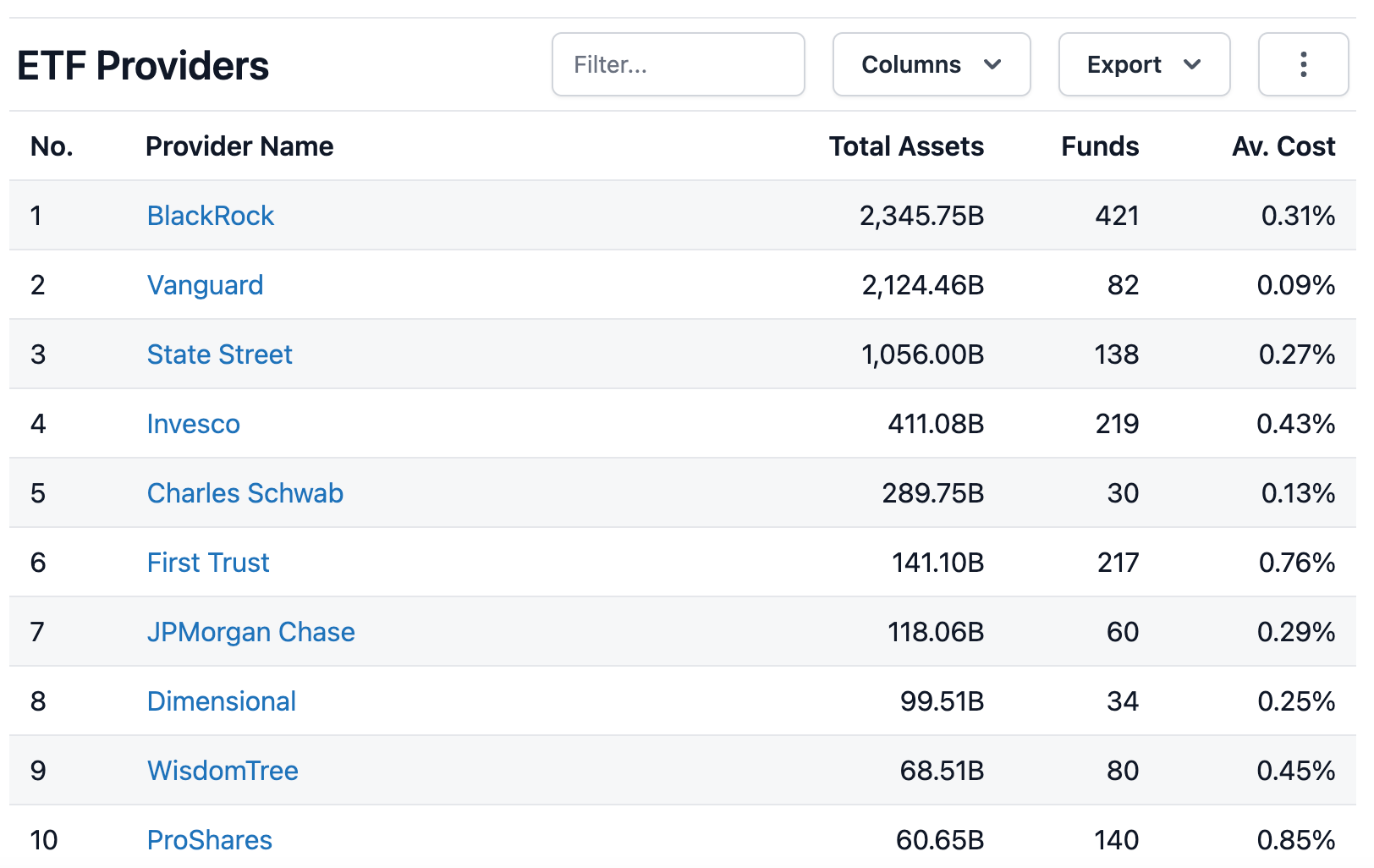

While a $4 billion ETF would be considered a huge success story for most other issuers, Vanguard operates with a different set of expectations. When 36 of Vanguard’s 82 U.S. listed ETFs have more than $10 billion in assets, $4 billion is considered a bit of a disappointment. In fact, VUSB only ranks as the 15th largest of the company’s 21 fixed income ETFs.

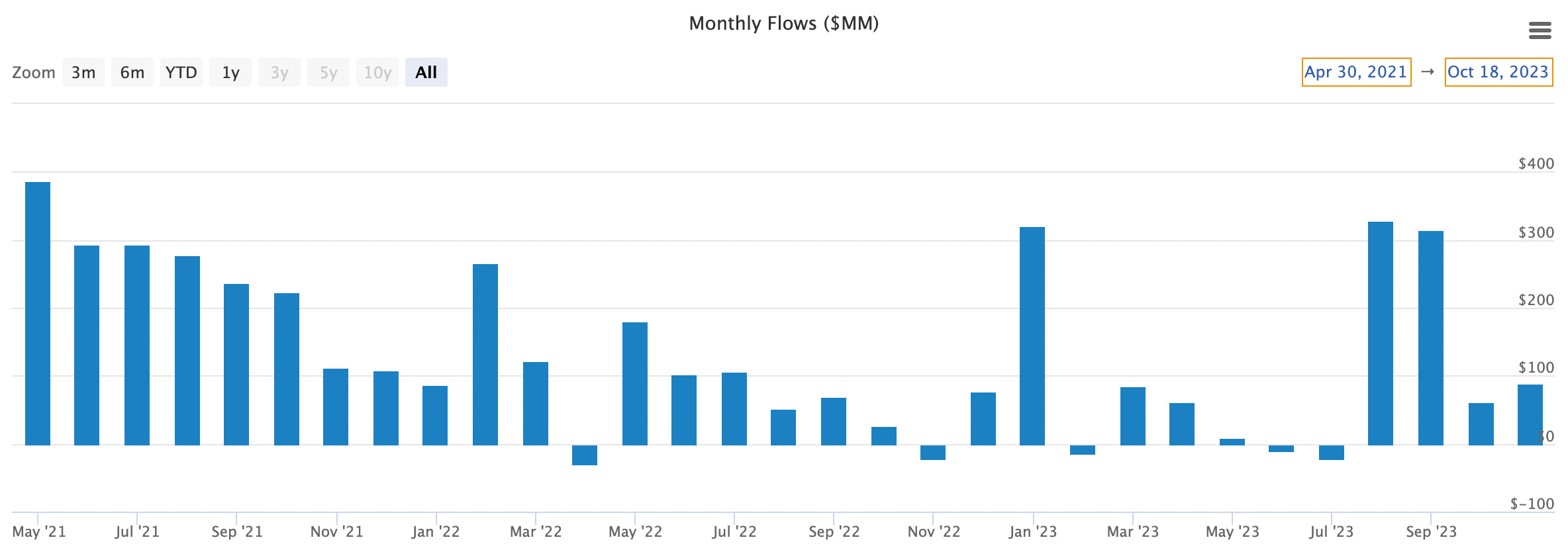

We can see from a flows perspective that while the fund came out of the gate pretty strong, investors largely lost interest within about a year.

This is a particularly concerning trend given that flows dried up right around the time that ultra-short bond and Treasury bill ETFs were picking up steam thanks to rapidly rising yields and downside protection. VUSB had a couple of relatively good months, historically speaking, recently, but it’s not too impressive given the sheer amount of money that’s flowed into this category over the past year. Still, VUSB isn’t closing shop anytime soon.

The bigger swing and miss has been Vanguard’s lineup of factor ETFs. These are the most “un-Vanguard” funds on its roster and its evident by the amount of assets they’re carrying that investors have largely ignored them. After more than 5 years, the entire suite of factor ETFs has just $1.4 billion in total assets. Some Vanguard funds have taken in that much money in a single day!

There’s nothing really fundamentally wrong with these funds. They tilt in the directions that they’re supposed to. The expense ratios are very competitive within the active factor ETF universe. They just don’t fit in with Vanguard’s brand. Think of it like McDonald’s adding healthy options to their menu. Sure, some people might like them, but most people don’t go to McDonald’s looking for healthy food. In Vanguard’s case, investors are looking for ultra-cheap index funds, not active factor funds.

This article runs down some of the challenges Vanguard has experienced with these ETFs, including manager departures and a lack of backing by the company in general. The factor ETFs did, however, manage to accomplish something that’s never happened before…

I mentioned earlier that Vanguard has launched 7 actively-managed ETFs, but only 6 appear in the graphic above. That’s because the company shut down its liquidity factor ETF roughly a year ago. Most of the remaining ETFs are large enough that they can remain viable on their own, but I wonder if Vanguard would consider just cutting bait on the experiment altogether and shut them down. Funds with more than $50 million in assets are rarely closed, but Vanguard is such a unique outlier that we may see something more unusual happen here.

Conclusion

Vanguard has built its success on low-cost index fund offerings, but it looks like that’s probably where its product lineup will stop. If investors are looking to add a thematic or niche ETF to their portfolio, they’re going to have to look elsewhere. Given the tepid (at best) response to their factor ETFs, it seems very unlikely that Vanguard is going to test the waters again outside of its core business model. That’s not necessarily a bad thing since Vanguard has done incredibly well for itself, but it’s likely going to be unable to offer investors everything they’re looking for in one place.

Great post!!