Small Cap Rally A Good Sign; Growth Replaces Cyclicals As The Market Leader

Consumer discretionary and tech stocks are overbought, while investors continue to dump gold.

After several weeks of lagging large-caps, the Russell 2000 posted a huge 6% gain last week as the bulls came out in full force. A strong jobs report coupled with a relatively dovish message on the taper launch from Jerome Powell continued to push investors out of cyclicals and back into growth sectors, such as tech and consumer discretionary.

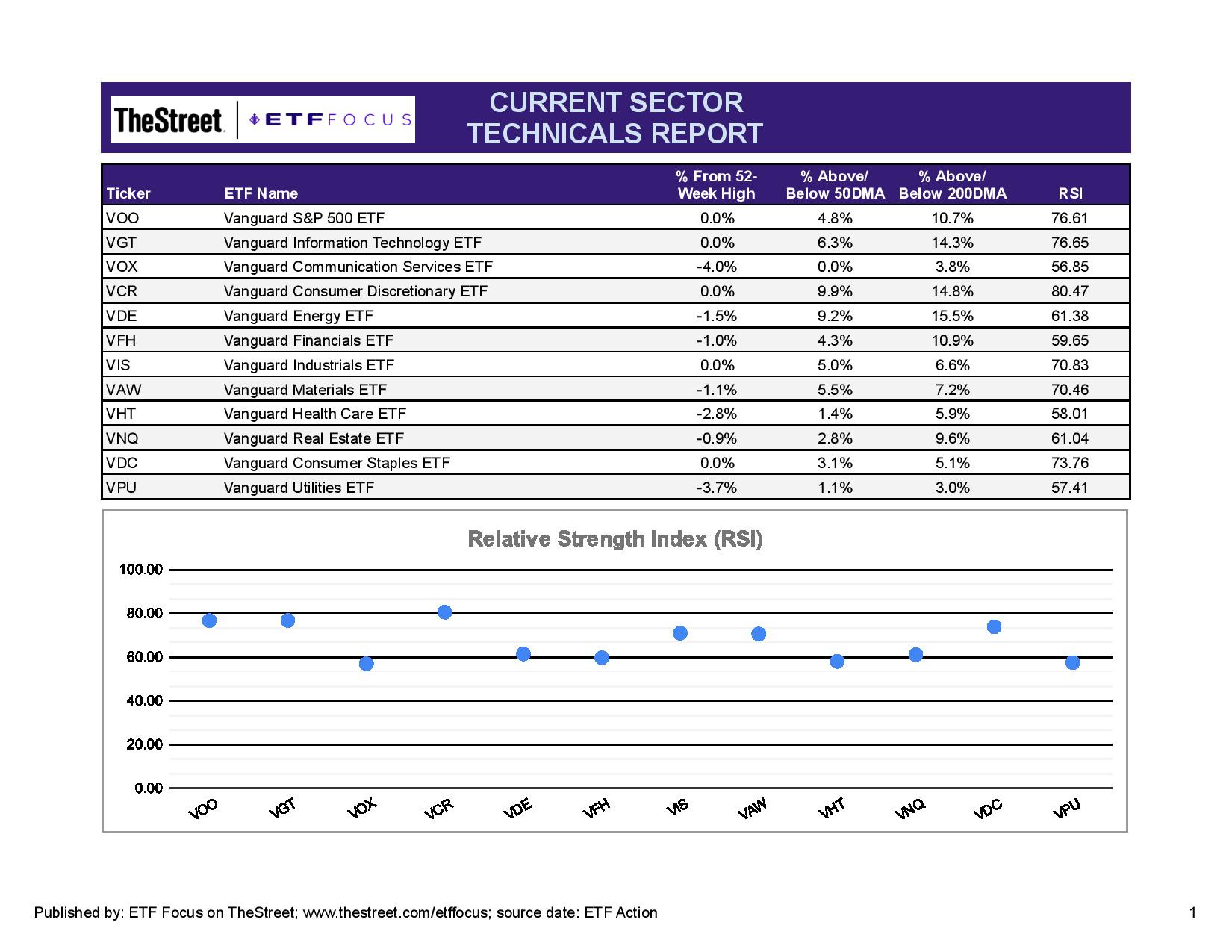

Over the past month, the S&P 500 is up 8% and the Russell 2000 is up 9%, but many sectors, including large-caps, mid-caps and small-caps are getting into overbought territory. Consumer discretionary stocks have been ripping, up 17% in the past month, but that sector along with tech look like they’re primed to take a breather. It’s a bit odd, however, to see those two sectors doing so well, while the tech-adjacent communication services sector languishes. Social media stocks, including Facebook, Snap, Twitter and Pinterest (if you consider that social media) have been the big drag as the ad revenue environment gets more challenging.

Utilities and healthcare are the weakest of the sectors, although they’ve still generated gains of 4-5% over the past month. Communication services is right at its 50-day moving average and one of the closest to crossing its 200-day moving average, so technicians should be aware. Cyclicals are generally still looking good although they’ve clearly cooled and ceded leadership to growth for the time being.

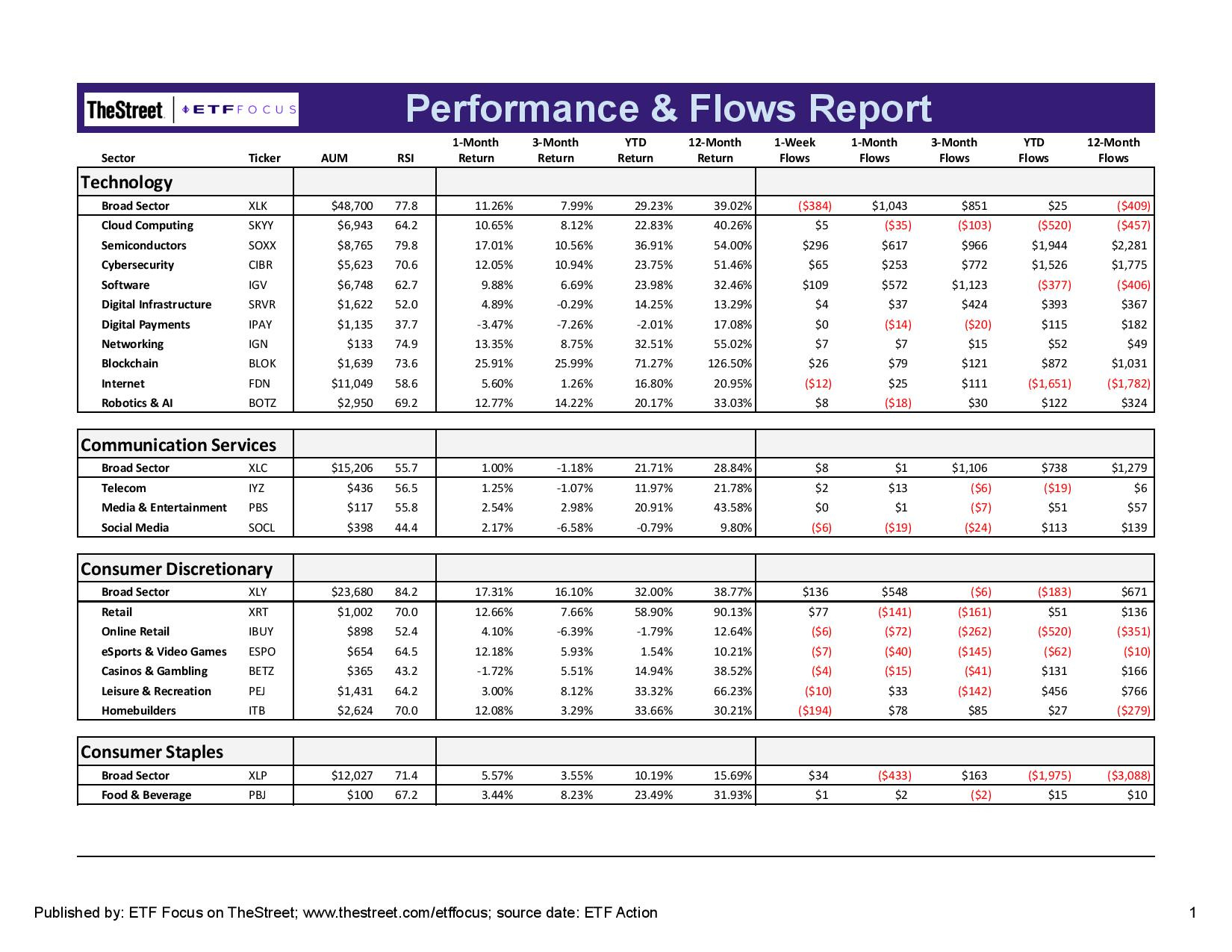

Tech continues to look strong, although overbought. Semiconductors are looking very strong here, with networking, cybersecurity and blockchain stocks driving gains. It’s interesting to note that there are some real pockets of weakness here under the surface. The digital payments sector has been very weak and is actually down 2% on the year. Flows into the sector have been solid over the past month as the sector rebounds, but somewhat surprisingly tepid over the year as a whole.

Social media is clearly driving the short-term weakness in communication services here, but traditional telecom names aren’t doing a whole lot better. The sector has been pretty much dead money over the past three months and investors have been largely ignoring it.

Strong retail sales and consumer activity despite high inflation and an uneven labor market recovery have kept the discretionary sector in the lead. Retail and homebuilder names continue to provide strength, although the sector appears to be a little top-heavy. Online retail, which had been the unquestioned leader in this area for several quarters, is beginning to come back down to earth as investors find traditional retail a better value. Leisure stocks have had a good but not great run.

Consumer staples, a little surprisingly, are in overbought territory despite consistently lagging this year. Defensive sectors remain out of favor.

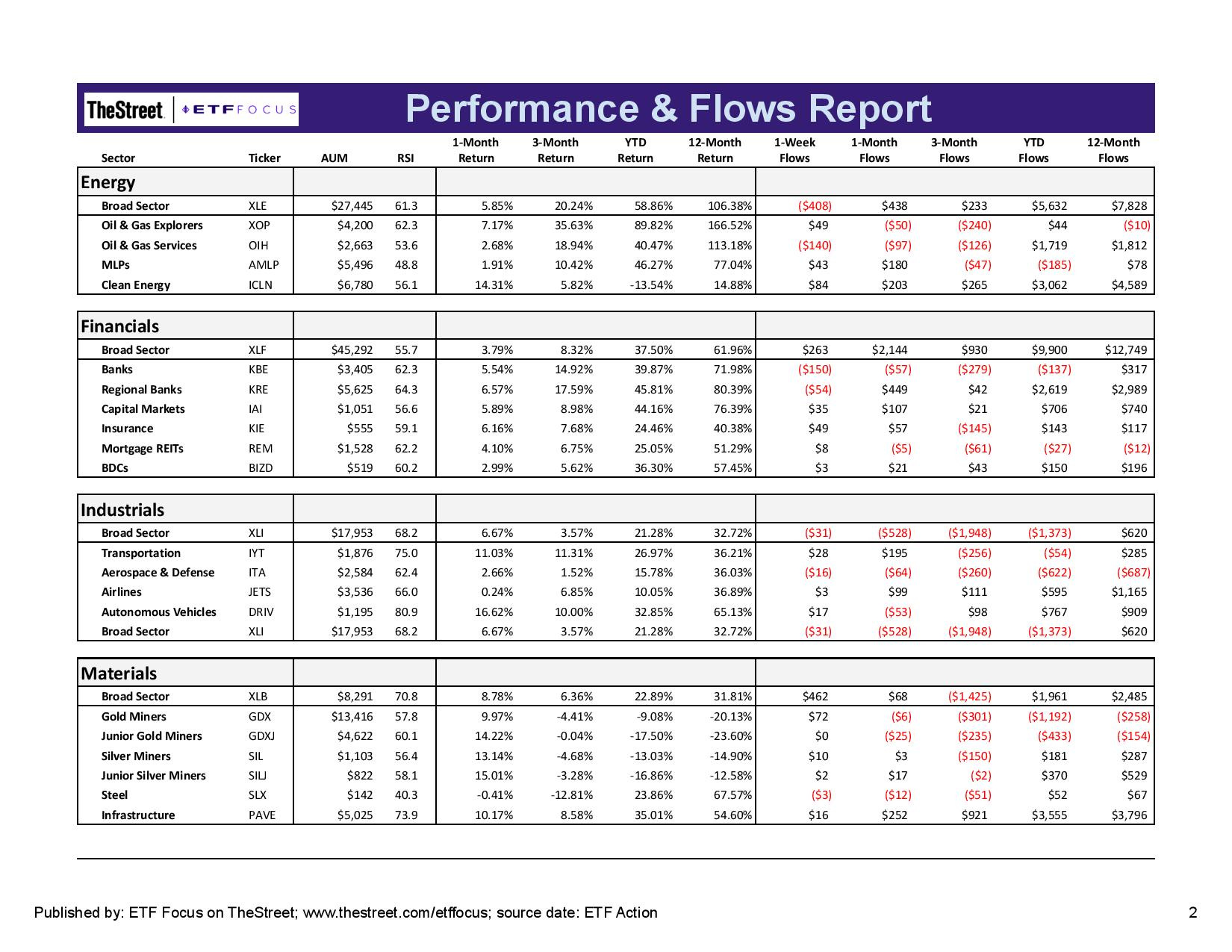

The bull market in energy stocks looks to be over in the near-term as the cyclical rally fades and crude oil prices retreat a bit. Clean energy has been a wild ride over the past several months, but investor money keeps flowing into the sector. This has mostly been a rally of traditional energy names.

Financials are also backing off following a strong run of outperformance. The banks, in general, have led this sector higher, but the biggest gains have come from the smaller regional banks. The flow data in 2021 shows that investors have also been following the trend. The Regional Banking ETF (KRE) has nearly tripled in size year-to-date.

Industrials and materials are still looking pretty good here. Autonomous vehicle stocks have done very well thanks to Tesla’s rally. Transports and infrastructure names are doing well. Steel is the one big laggard as industrial commodity prices have been incredibly volatile. Lumber and copper prices are both well off of their recent highs.

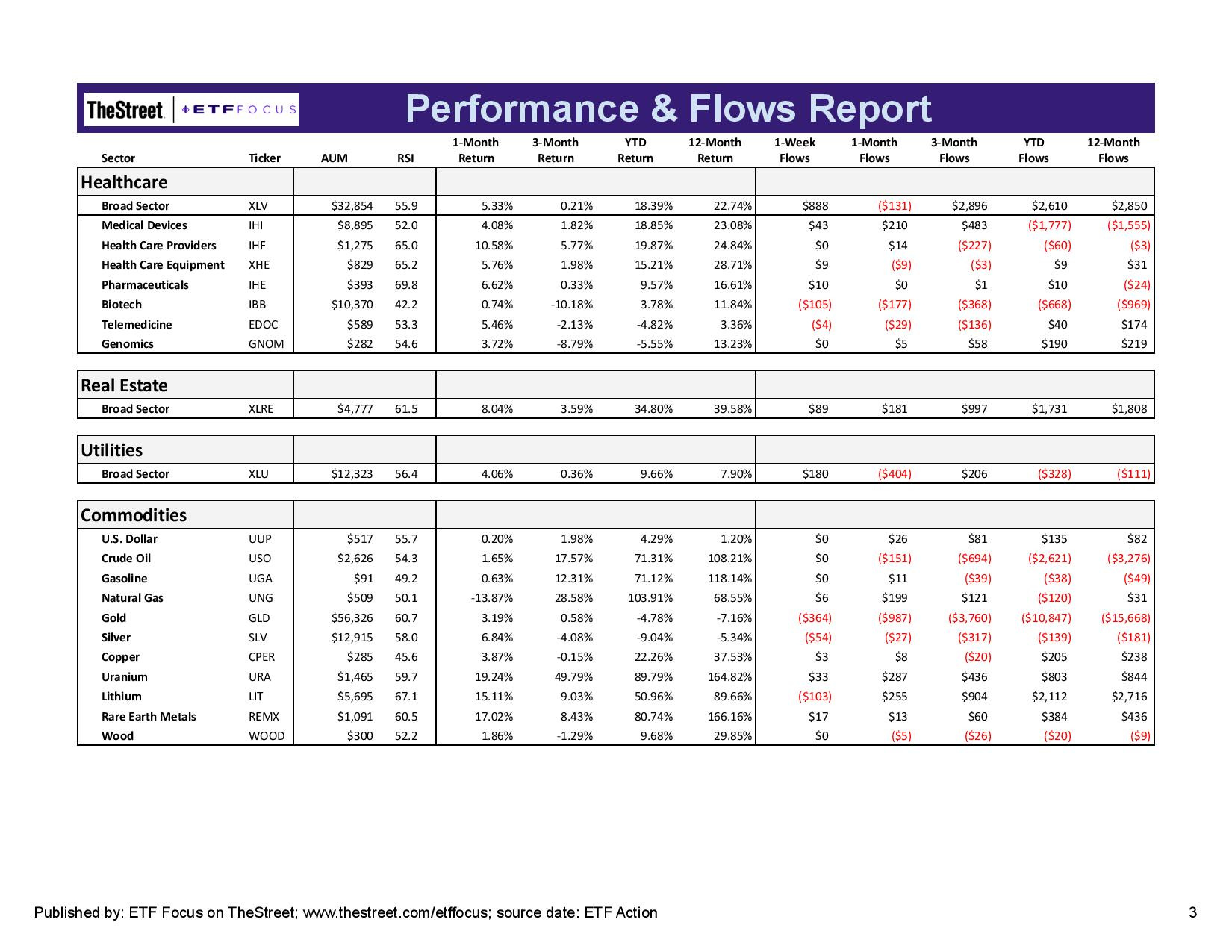

Healthcare, real estate and utilities look set to keep trailing the market, although REITs may be the exception. It’s still one of the best-performing sectors of 2021 even though it’s underperformed along with other defensive sectors over the past few weeks. The infrastructure bill passage should provide at least a modest boost to subsectors, such as data center, infrastructure and industrial REITs, although residential real estate and office buildings could be a mixed bag. Pharmaceuticals and healthcare providers have looked strong lately, but they’re the exception to the rule.

Energy prices, including crude oil, gasoline and natural gas, are coming back down off of their highs and have given up most recent strength. There’s still some money coming into nat gas, but crude oil has seen some significant outflows. The big story, however, remains gold where investors keep running for the exits as inflation fails to ignite a meaningful rally.

Read More…

5 Dividend ETFs For November 2021

Worst Performing ETFs For October 2021

Top Performing Dividend ETFs For October 2021

Top Performing ETFs For October 2021

Why I'm Still Choosing GBTC Over BITO For Bitcoin Exposure

LIVE BLOG: Bitcoin ETF Launch Day

ETFs of CEFs: Up To 9% Yields Available For Income Investors

ETF Battles: Which Bond ETF Is The Better Strategy For Rising Interest Rates? - FLOT vs. IVOL

ARKK vs. ARKW vs. ARKF: Which ARK Disruptive Tech ETF Is Better?

Questions, Ideas, Thoughts?

Feel free to reach out by replying to this e-mail or commenting below. Your question or idea might be used in a future newsletter!