Private Equity ETFs Could Be the Next Major Retail Investing Mistake

Product complexity and a lack of underlying liquidity could badly hurt investors who don't understand these things.

For years, private equity and private credit were largely reserved for institutions, pension funds, endowments, and ultra-wealthy investors willing to lock up capital for years at a time.

Not any more.

A growing number of ETF issuers and asset managers are now racing to bring private markets into ETF wrappers. The pitch is enticing. Everyday investors can finally gain access to the same private investments once reserved for the institutional elite.

In theory, that sounds like democratization.

In practice, it may be introducing a level of liquidity risk and unclear valuation that many retail investors don’t fully understand.

This is quickly becoming a huge structural risk for these ETFs.

The Fundamental Liquidity Mismatch

Traditional ETFs work beautifully because the underlying assets are liquid.

If you own the Vanguard S&P 500 ETF (VOO), for example, the fund holds stocks that trade continuously during market hours. Authorized participants can create and redeem ETF shares efficiently because the underlying holdings have transparent prices and active markets.

Private equity doesn’t work that way.

Many private investments:

Don’t trade daily

Have no transparent market price

May require months or years to sell

Depend heavily on appraisal-based valuations

Often rely on negotiated transactions rather than open-market pricing

That creates a serious structural issue.

The ETF wrapper promises daily liquidity to investors. The underlying assets usually can’t realistically provide it.

That mismatch becomes dangerous during periods where the markets turn volatile.

The Warning Signs Are Already Here

Several areas of private market investing have already shown signs of stress.

During the 2022-2023 rate shock, multiple private real estate and private credit funds experienced redemption pressures and gating mechanisms.

One of the most notable examples involved Blackstone and its private credit fund (BCRED) vehicle. Investors requested more withdrawals than the fund could reasonably provide in its illiquid securities. It managed around the situation by raising capital to fund redemption requests, but it’s NOT business as usual.

BCRED was not an ETF, but the event highlighted a broader issue. Just because ETF shares may be liquid doesn’t mean that the securities within the ETF are.

If anything, the liquidity expectations become even more potentially problematic because ETF investors are accustomed to instant liquidity and tradability.

The ETF Can Create an Illusion of Liquidity

This may be the single biggest risk retail investors fail to appreciate.

In normal markets, ETF liquidity often appears abundant because buyers and sellers offset one another. But during panics, the ETF structure ultimately depends on the liquidity of the underlying holdings.

If the underlying private assets cannot be sold efficiently, several problems can emerge:

Wider bid-ask spreads

Significant discounts to net asset value (NAV)

Trading halts

Forced asset sales

Valuation uncertainty

Increased tracking error

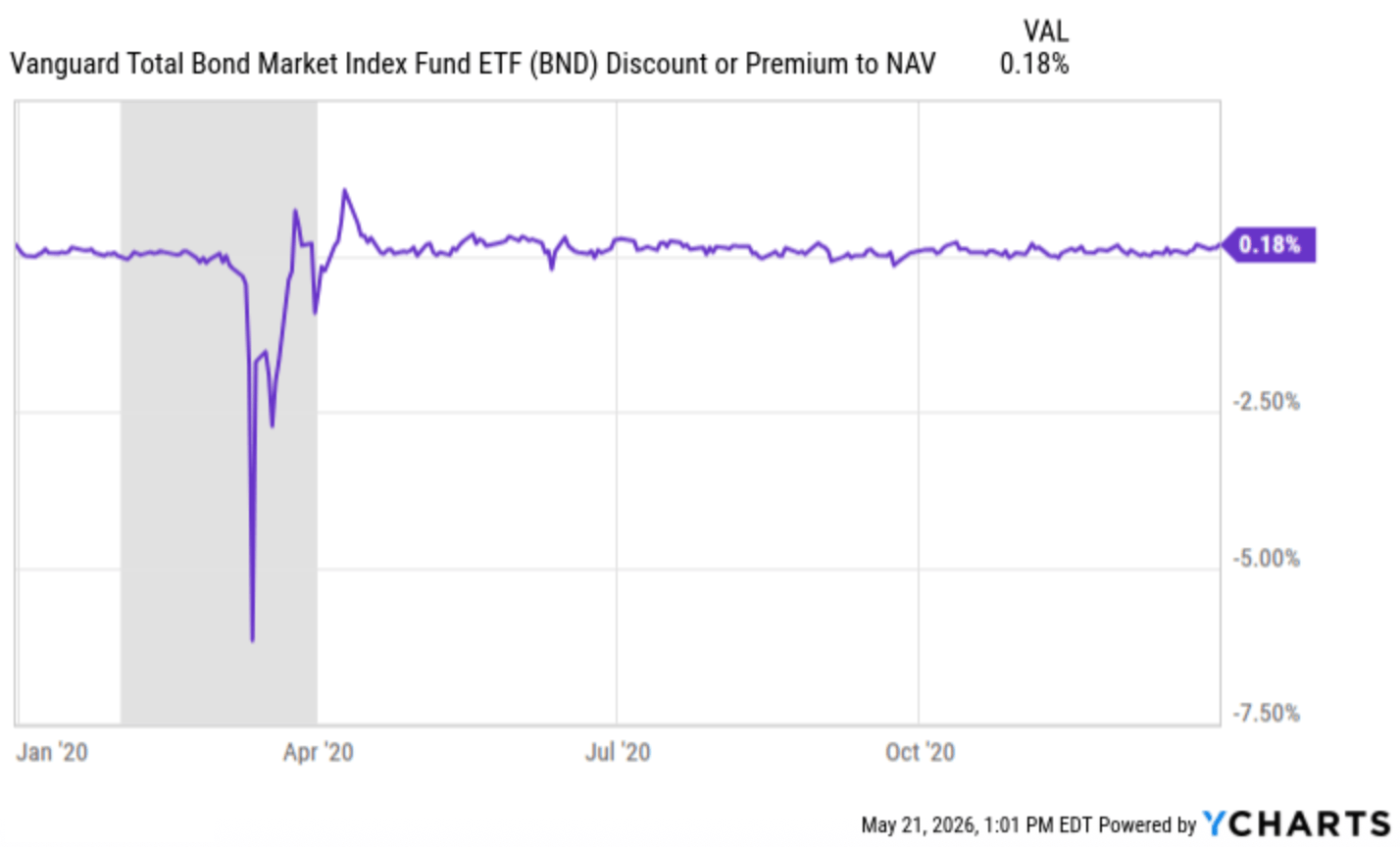

Investors saw glimpses of this dynamic even in relatively liquid bond ETFs during March 2020.

Even huge ETFs, such as the Vanguard Total Bond Market ETF (BND), saw share prices deviate significantly from their NAVs, something that rarely happens in the ETF world.

Now imagine a similar environment involving hard-to-price private loans or private equity stakes.

The stress scenarios become much more severe.

Valuations Are Far Less Reliable Than Investors Assume

One reason private assets often appear “less volatile” than public markets is because they are not marked to market continuously.

This can create the appearance of price stability where it doesn’t actually exist.

But smoother does not necessarily mean safer.

In many cases, private assets are valued using models, appraisals, comparable transactions, or manager estimates. Those valuations can lag reality significantly during rapidly changing economic environments.

This can create a dangerous psychological effect: Investors may believe private assets are stable precisely because the pricing mechanism updates slowly.

Public markets force investors to confront volatility immediately. Private markets often delay that recognition.

In a severe downturn, repricing can happen all at once and in a way that can hit investors hard.

Retail Investors May Not Understand What They Actually Own

Another growing concern is complexity.

Many of these products market themselves using broad labels like:

“Private markets”

“Private credit”

“Alternative income”

“Enhanced yield”

“Institutional opportunities”

Those terms sound sophisticated and attractive. But underneath the surface, investors may be exposing themselves to:

Leveraged middle-market loans

Venture-backed companies with uncertain valuations

Distressed debt

Real estate development financing

Illiquid secondary market positions

Credit structures with few covenants

That is a dramatically different risk profile than many traditional ETFs.

Yet the ETF wrapper can psychologically make the product feel safer and more familiar than it actually is.

Private Credit Risks Are Growing Quickly

Private credit deserves particular scrutiny.

Over the past decade, banks pulled back from portions of corporate lending due to regulation and balance sheet constraints. Private lenders stepped into the gap aggressively.

The result has been explosive growth and the private credit market is now valued in the trillions of dollars.

In good economic environments, this has looked brilliant. It’s resulted in:

Higher yields

Floating rate exposure

Strong performance

Low visible volatility

But much of this growth occurred during an unusually favorable credit environment.

A prolonged recession could expose a number of vulnerabilities at the same time, such as:

Rising defaults

Weak recovery values

Refinancing stress

Reduced deal activity

Liquidity troubles

Many private loans have never been truly stress-tested through a deep and prolonged credit cycle under today’s rate structure. A lot of ETFs could be in line to experience major declines if this were to happen today.

Asset Managers Have a Financial Incentive To Sell These Products

The economics behind these products also deserve skepticism.

ETF issuers are facing enormous pressure to differentiate themselves in an overcrowded market.

Launching another plain-vanilla S&P 500 ETF is unlikely to generate meaningful asset growth since that market is already saturated. Single stock and ultra-high yield derivative income strategies were the most recent major wave. A niche AI-related ETF boom is happening right now. Private market ETFs are picking up momentum along side them.

Private markets, however, offer something incredibly attractive to asset managers: higher fees.

Traditional broad-market ETFs now compete near zero expense ratios. Alternative products do not.

That creates a powerful incentive for Wall Street firms to package increasingly complex and less liquid strategies into vehicles that appear accessible to retail investors.

There are no shortage of historical examples demonstrating that when financial engineering collides with aggressive fee incentives, investors should proceed carefully. Just look at how the financial crisis played out.

The Next Crisis Could Reveal Problems Retail Investors Aren’t Aware Of

Many risks remain hidden during bull markets.

That is especially true in private assets because valuations move slowly and liquidity assumptions are rarely tested aggressively until panic arrives.

The danger is not necessarily that these products fail tomorrow. The danger is that investors misunderstand the risks for years before the real stress event occurs.

That pattern has happened repeatedly throughout financial history:

Mortgage-backed securities before 2008

Volatility-linked ETNs before 2018

Certain bond funds during liquidity panics

Gated real estate vehicles during stress periods

The common thread is usually the same. Investors believed liquidity existed until everyone wanted out simultaneously. Then it didn’t.

But Private Markets Aren’t Worthless

Private equity and private credit can absolutely play useful roles in sophisticated portfolios.

Institutions allocate heavily to these areas for valid reasons:

Diversification

Yield enhancement

Access to non-public growth opportunities

Potential illiquidity premiums

But institutions also:

Conduct extensive due diligence

Use long investment horizons

Understand liquidity constraints

Stress-test scenarios aggressively

Maintain diversified funding structures

Retail investors often do not have those advantages. That is what makes the rapid ETF growth in private asset products potentially concerning.

Bottom Line

The ETF industry has delivered enormous benefits to investors over the past two decades. Lower costs, tax efficiency, transparency, and accessibility have fundamentally improved portfolio construction.

But not every asset belongs inside a daily liquidity wrapper. That may become one of the defining lessons of the next market cycle.

Private equity and private credit ETFs could eventually succeed in creating broader access to alternative investments. But they may also introduce structural risks that many investors are badly underestimating today.

The biggest danger is the possibility that the ETF wrapper creates a false sense of simplicity, liquidity, and safety around investments that remain inherently complex and illiquid underneath the surface.

It makes sense conceptually but that doesn’t mean it makes sense for most retail investors no ?

The daily‑liquidity ETF wrapper around inherently illiquid assets is the real issue. Retail investors are used to clicking “sell” and getting out instantly. Private equity doesn’t work that way.

If you don’t fully understand liquidity risk, valuation lag, and credit cycles, this probably isn’t the place to experiment.