Inflation Catches Markets Off-Guard; Gold Finally Shines Again

Investors continue to dump Treasuries as financial markets reset expectations.

For a while, the inflation narrative was “rising, but transitory”. Then it shifted to “rising, but not quite so transitory”. After last week’s October report, the narrative has to be “rising faster than expected and we don’t know when it’s going to stop”.

The markets had been pricing in high inflation rate expectations for a while (the bond market more so than equities), but even last month’s print of 6.2%, the highest in more than 30 years, caught the markets off guard. If you look at the broader market averages - the S&P 500 was down 0.3% last week, while small-caps fell about 1%, you might not think it was that big of a deal, but the bigger deal came in how other asset classes reacted. Treasury yields shot higher, gold prices rose nearly 3% and the dollar hit its highest level since July 2020. Equities continue to sit in kind of this goldilocks position of constant net flow support and low volatility, but other asset classes are demonstrating a reset of sorts below the surface.

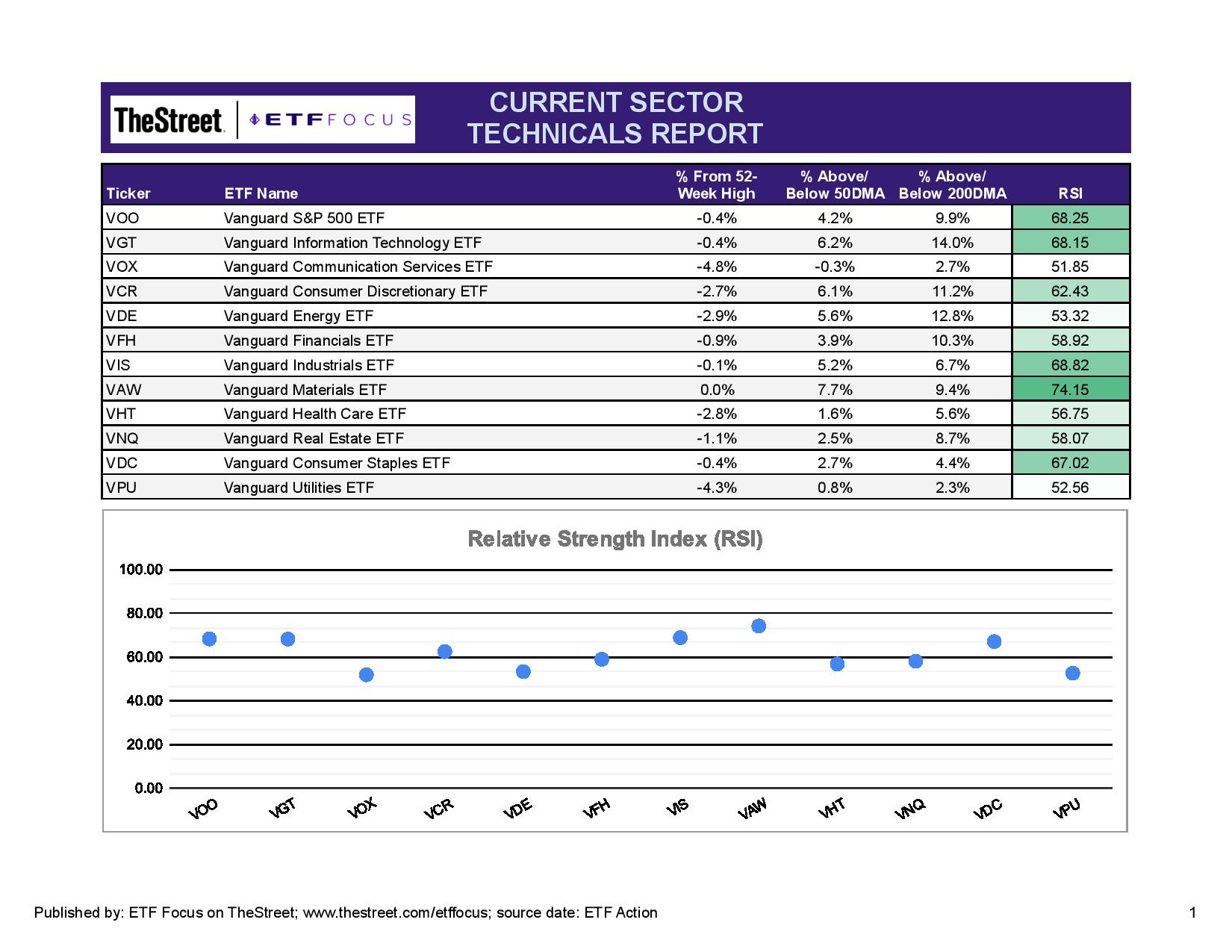

Let’s start our weekly review by taking a look at the primary market sectors.

Relative strength has cooled somewhat following last week’s pullback, but there’s still nothing at the moment that’s looking particularly weak on an absolute basis. Tech has seen perhaps the biggest resurgence over the past few weeks and has begun leading this market once again. In terms of growth sectors, it’s been starting to go it alone though. Consumer discretionary, which had been one of the market’s best-performing sectors, took a big step back last week amid concerns about retail sentiment and inflation. Communication services continues to be a big laggard and is getting dragged lower by social media stocks.

Cyclicals rebounded last week led by a huge 2-3% rally in materials stocks. Industrials and financials also had a good week, but the energy sector continues to cool off as high inflation is seen as cooling economic demand. Defensive sectors continue to mostly underperform. REITs are still looking fairly positive as rental rate increases are seen as one of those stickier sources of inflation. Consumer staples look relatively strong on the surface, but have underperformed the market consistently pretty much ever since the COVID recession. Utilities has been a steady laggard since August.

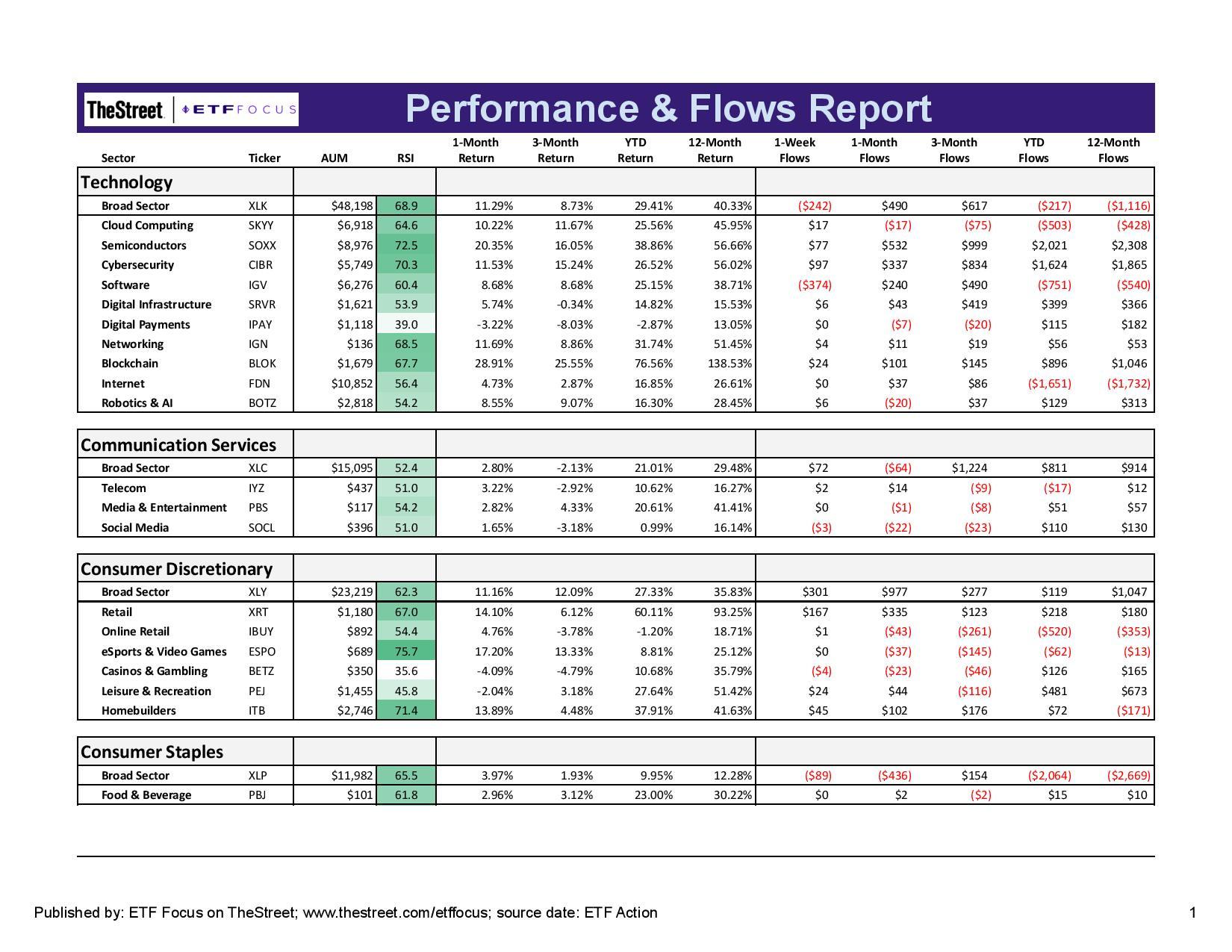

Tech continues to look strong, although net flow activity shows that investors haven’t been reacting in a major way. Semiconductors and blockchain remain red hot, both gaining more than 20% over the past month alone. Digital payments stocks still look really weak and there hasn’t been much momentum in the internet stock space either.

Communication services, again, is one of the worst-performing sectors lately, but it does look like things might be balancing themselves out. Social media looks like it might be in the early stages of turning higher, but traditional telecom and media names haven’t generated any excitement.

On a longer-term basis, consumer discretionary is still looking positive, although last week was a setback. The clear laggards in this group are the leisure & entertainment plays. The catalyst, of course, being inflation and slowing demand for hotels, travel, etc. amid higher costs. The video game sector showed strong sales growth again last week and that’s lifted this group higher. Homebuilders are still looking good, but watch for retail both this week and through the holidays.

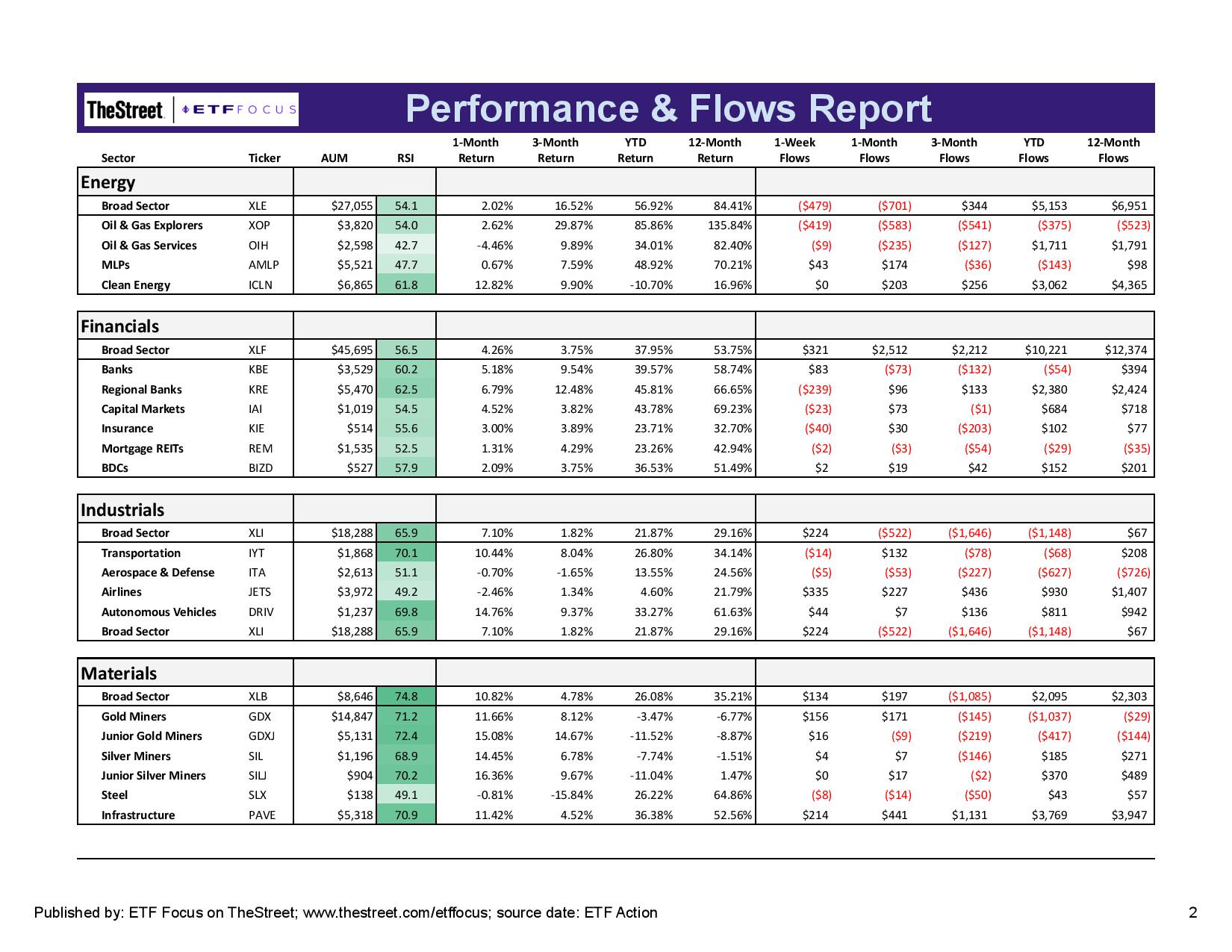

There’s still a dichotomy between traditional fossil fuel energy and clean energy stocks. Crude oil prices are off their highs, but still elevated at around the $80 a barrel level. Net flows, which had been pouring heavily into this sector have now reversed course and are moving back out again. Hydrogen has been a particularly strong theme within the clean energy space.

Financial stocks are pretty consistent across the board with no single subsector really outperforming. Banks had been and still are leading slightly, but there’s no real advantage in terms of short-term relative strength. The higher interest rate narrative appears to be bringing investors back into the fold and with the pressure continuing to build for move rates higher still, I think there’s more potential return ahead in this group.

Industrials and materials have been big beneficiaries of the recent resurgence in cyclicals. Investors still aren’t treating these as actionable plays and continue to focus mostly on tech, energy and financials as trading options. Airlines have dragged somewhat along with the weakness in other leisure sectors, but precious metals miners are picking up strength here following last week’s inflation-inspired bounce. Whether this group can continue this short-term run after performing miserably for virtually this entire year will likely depend on where inflation heads from here.

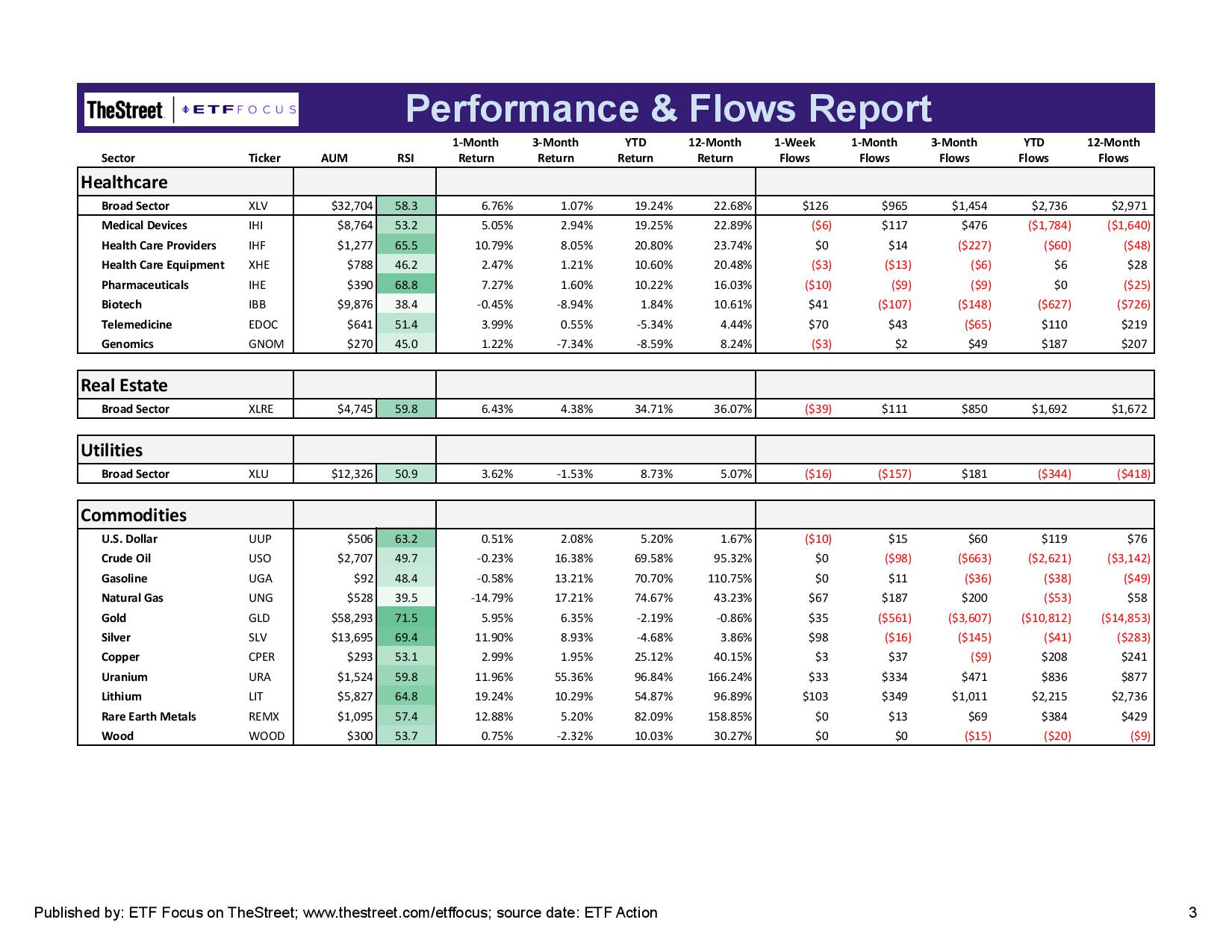

Not a whole lot of action on the defensive sector side. Biotech remains a notable laggard as has been the case throughout the year. Pharmaceuticals and healthcare providers are also looking relatively strong, but with prescription drug pricing appearing to be back on the agenda following the signing of the infrastructure bill, there might be some downside pressure ahead.

Gold and silver are obviously the biggest movers recently as I just mentioned above. Nat gas prices continue to come back down and remain the weakest of the commodities right now. Rumors that the White House may begin tapping the Strategic Petroleum Reserves could put short-term pricing pressures on oil, nat gas and gasoline prices, but I expect demand to remain firm through the winter months.

Read More…

ETF Battles: Looking For The Best Bitcoin ETF - BITO vs. GBTC

The Short ARKK ETF Launches For All The Cathie Wood Haters

5 Dividend ETFs For November 2021

Worst Performing ETFs For October 2021

Top Performing Dividend ETFs For October 2021

Top Performing ETFs For October 2021

Why I'm Still Choosing GBTC Over BITO For Bitcoin Exposure

LIVE BLOG: Bitcoin ETF Launch Day

ETFs of CEFs: Up To 9% Yields Available For Income Investors

Questions, Ideas, Thoughts?

Feel free to reach out by replying to this e-mail or commenting below. Your question or idea might be used in a future newsletter!

one of the few information email from "The Street" that I enjoy. Keep up the good work.

JEPI is always optimistic. :)