ETF Focus Rewind: Two Themes Within Tech That Investors Should Target

Tech stocks are starting to come back, but a pair of groups within the sector look particularly attractive.

2 ETFs To Consider Buying (And 1 To Avoid) This Week

With the release of the minutes from the Fed's July policy meeting last week, the word "taper" officially becomes a big part of the market narrative for the remainder of 2021. The central bank indicated that the majority of its members would currently be on board with the idea of tapering its bond purchases before the end of the year. The news didn't really come as a big surprise since most market participants have expected that the Fed will begin backing off of bond purchases sometime over the next 2-3 quarters. Equities, however, sold off on the release and never recovered as the S&P 500 finished down about 0.6% on the week and small-caps fell 2.5%. Treasuries again posted modest gains with the 10-year yield finishing around the 1.26% level.

Attention now turns to the Jackson Hole summit later this week where the Fed members will convene to discuss all manner of policy, but the topic of when tapering might begin will clearly be the focus. To be clear, there's no guarantee that we'll even get a definitive answer and there's a possibility that Jerome Powell in his Friday speech will continue to only speak in general terms about the idea of tapering. With the delta variant continuing to threaten the economic recovery and recent weakness in both retail sales and consumer sentiment, the Fed may take a wait-and-see approach to its tapering calendar before committing to an actual timeline.

Have conditions improved enough to warrant a bond tapering? I think the overall answer to this question is "yes", but there are certainly pockets of weakness and questions that need to be monitored. The PCE rate, the Fed's preferred measure of inflation, is currently 4% year-over-year, so it looks like the central bank's inflation requirement has been met, even if some of the short-term price increases turn out to be transitory.

The unemployment rate is back down to 5.4% following an add of nearly one million jobs in July. While there is still some labor market slack, the eventual expiration of enhanced unemployment benefits and the start of the new school year could ignite the return of more normal labor conditions. With jobs plentiful, wages increasing and little indication at this point that businesses will re-close, the labor market seems to be in good shape and should be able to handle a withdrawal of central bank support.

I think it's important to point out here that the Fed won't necessarily be tightening policy as much as it'll be loosening it less. Right now, the central bank is buying a combined $120 billion of Treasuries and mortgage-backed securities monthly. That number would only be reduced by an as-of-yet unknown amount in the initial steps of tapering. It will continue buying bonds and injecting liquidity into the economy, so this will be a very gentle first step in a return to economic normalcy. Every recent attempt by the Fed to tighten policy has eventually been met by higher volatility and falling stock prices and I doubt it has forgotten what happened when it tried to normalize rates back in 2018. I think last week's even modest sell-off in stocks is an indication that investors are nervous about the Fed withdrawing its support. The outperformance of utilities and consumer staples over the past month along with the steady gains in Treasuries suggest that there's a broader defensive pivot taking place right now.

A taper during the 4th quarter of this year could end up being a case of bad timing that could spike volatility. Consumer sentiment is falling. Retail sales activity has weakened as consumers show a little more restraint in the face of rising COVID outbreaks. China's decision to reimplement social and economic restrictions could have global implications as the recent closure of its seaports could result in more supply chain issues worldwide.

Overall, I think U.S. large-cap equity prices are looking vulnerable here and taper talk could be a catalyst to send share prices in reverse. Keep in mind also that the government debt ceiling has been hit and there's still no resolution in sight (or even discussion at this point) as Treasury cash balances keep getting taken down in the meantime. We know that the debt ceiling will eventually be lifted, but it's difficult to see how U.S. government creditworthiness will remain intact following what's likely to be an ugly battle getting there.

With that being said, here are three ETFs I'm going to be watching this week and the narratives that go along with them.

ETFMG Prime Mobile Payments ETF (IPAY)

Fintech represents a huge opportunity for innovation in the financial services space. Cryptocurrencies, such as bitcoin and ethereum, certainly occupy a piece of this industry, but the space is evolving far beyond that. Most think of credit card issuers, such as Visa and Mastercard, when they think of mobile payments, but other companies, including Square, PayPal, Global Payments Inc. and a number of foreign companies you may not have even heard of, are driving the migration towards a cash-less society.

The mobile payments sector, however, has been an underperformer. It's trailed the broader tech sector over every annualized time period since its inception, but 2021 has been especially rough. Both tech and the S&P 500 are up around 18% year-to-date, but IPAY has returned a scant 3%. You can see in the chart above that while the group rallied strongly off of the COVID bear market bottom, it's largely moved sideways since January. The economic recovery narrative, which had been intact for most of last year, has cooled as concerns about peaking growth and weaker consumer spending activity are putting a bit of a damper on the sector's outlook.

We've seen the consumer discretionary sector lag over the past several weeks since questions remain about the sustainability of sales growth in light of rising inflation and a lack of stimulus cash. While not directly affecting the sector, the indication from the Fed that it's likely going to be pulling its monetary support of the economy adds another reason to be cautious here.

Still, I like the cash-rich nature of these businesses and their ability to continue to generate cash flows in varying economic environments. In this sense, they have some defensive properties even though they are cyclical in nature. IPAY is also demonstrating relatively good value at the moment as well. Its trailing 12-month P/E ratio is slightly higher than that of the tech sector, but its price/sales, price/book and price/cash flow ratios are all significantly lower at the moment.

If you're looking for exposure in the tech sector, but want to target some of the more attractive short-term opportunities, I think the mobile payments space is a good option.

Global X Cybersecurity ETF (BUG)

Cybersecurity is one of those sectors that looks like it's always going to have a steady level of demand. Even as companies invest millions, if not billions, of dollars in protecting data and customer privacy, we're still seeing hackers get past firewalls and gaining access to personal information. Just recently we've learned of the data breach at T-Mobile, which is estimated to affect 53 million customers. The State Department was reportedly just hit with a cyber attack as well and let's not forget the case of JBS, the meat company that paid hackers $11 million in a ransomware attack. This problem isn't going away and investors have taken notice.

There are a number of cybersecurity ETF options available, but BUG looks like the best of the bunch even though it's one of the smaller funds in the space. Just like IPAY, BUG has struggled to gain traction throughout 2021 even as the tech sector keeps moving higher. It's returned only a modest 4% year-to-date as it's struggled multiple times to both break through and stay above the $30 level.

While the sector looks interesting here based on the optics of cyberattacks and anticipated demand for services, BUG represents perhaps the best option in the space due to its concentrated and targeted exposure. You've got 5%+ exposure to all of the industry's biggest names, including Zscaler, Fortinet, Palo Alto Networks, CyberArk and CrowdStrike. That's usually a red flag in my opinion, but in narrower niche industries, I think you want the highest, purest exposure possible, even if it means a higher concentration.

BUG may struggle if economic concerns continue to rise, but the strong demand narrative is there.

Consumer Discretionary Select Sector SPDR ETF (XLY)

It's worth repeating that the consumer discretionary sector looks vulnerable here. This group's success has been heavily dependent on an abundance of Fed liquidity. Not only have the stimulus checks stopped, ending an important source of consumer spending strength, it's looking like the Fed is getting ready to begin withdrawing some of its support for the economy. Granted, it's only going to be buying fewer Treasuries than it did previously, but the equity markets tend to respond negatively every time the words "taper" or "tightening" get mentioned.

With inflation making the costs of everything from gasoline to groceries higher and overall retail sales starting to weaken (although the online channel is still looking OK), consumer sentiment has taken a big hit and we're seeing evidence that shoppers are beginning to tighten the purse strings a bit as the delta variant spreads.

If you're looking to invest in the consumer space here, staples seem like the better play. I'd keep an eye on cyclicals here to get a sense of how investors are responding to the economic recovery story. If cyclicals continue underperforming here, as they have for the past several weeks, I'd expect to see continued weakness in discretionary stocks as well. We need to see signs of improved consumer confidence again before I'd consider reentering this sector.

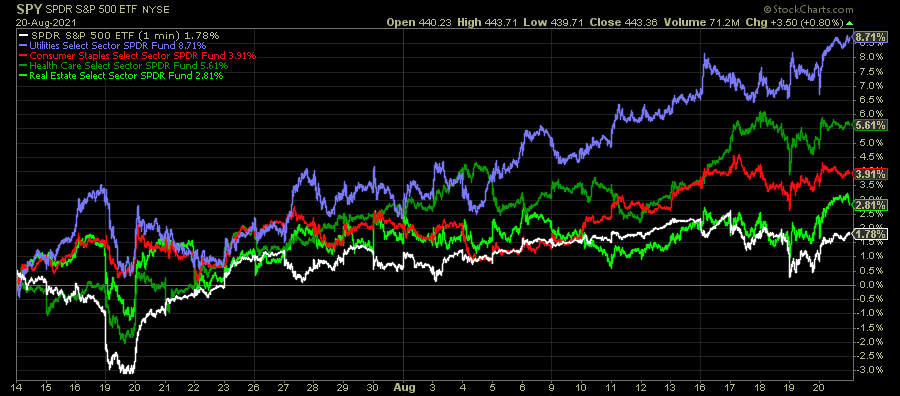

Chart of the Week

I’ve talked about how the markets have been turning defensive while breadth has been narrowing and I think this chart sums it up pretty well. Going back to the middle of July, it’s not the growth or cyclical sectors that have been leading, but the defensive ones.

We’ve seen all sorts of evidence of investors turning cautious here. Small-caps have been significantly lagging large-caps, while Treasuries continue to deliver gains despite equities moving higher. Gold continues to move sideways as investors remain unconvinced that inflation risk is more than temporary. It’s the behavior of defensive equities, however, that might be telling the more compelling story.

Let’s start with the utilities sector, which has outperformed the S&P 500 by 7% over the past several weeks. Utilities have actually been outperforming the broader market going all the way back to June, but it’s this latest run since mid-July that’s been the most convincing due its steadiness. Consumer staples, which have steadily underperformed since the market bottomed back in 2020, are even getting pulled higher in this defensive shift. When these two sectors start moving higher together, there’s usually an underlying tone of caution that’s growing.

Healthcare is another sector that’s been performing very well since June. With COVID cases still growing, a lot of focus has returned to higher consumer healthcare costs over the coming year. Drug pricing is something that hasn’t come to the table yet despite much discussion in the past. Earnings growth has been solid for this sector over the past year and that’s helped push this group higher.

Real estate has been one of the best performing sectors all year. The reopening economy has improved demand and income prospects for all manner of industry - retail, office space, infrastructure and rental properties among them. August has seen this sector move sideways as the bullish factor with respect to the reopening trade is wearing off.

But this is a convincing move for defensive equities as a whole. When you get a pair of these sectors outperforming for an extended period of time, it’s worth monitoring closely. When all of them have been outperforming the broader market for the past five weeks, it could be a warning sign.

Read More…

The Simple 4 ETF Retirement Portfolio

2 Vanguard ETFs To Power Your Global Dividend Growth

ETF Battles: DVY vs. TLT vs. VNQ - Which Dividend Income ETF Is Better?

2 ETFs To Consider Buying (And 1 To Avoid) This Week

Grayscale Plans On Converting GBTC To An ETF; Here's Why That's Not A Good Idea

ETF Battles: CTEC vs. PBW vs. TAN - Which Clean Energy ETF Do You Buy?

Tuttle Files For A Short ARKK ETF

Questions, Ideas, Thoughts?

Feel free to reach out by replying to this e-mail or commenting below. Your question or idea might be used in a future newsletter!