ETF Focus Rewind: A 5% Dividend Yield On Top Of The S&P 500

This week's edition also looks at inflation stocks, Chinese tech and the Fed's history of tapering.

2 ETFs To Consider Buying (And 1 To Avoid) This Week

You have to give Jerome Powell some credit. In last week's Jackson Hole speech, he managed to set the tone for asset purchase tapering while making investors feel good about the idea.

Last week, stocks did an abrupt about-face even before the Fed's big gathering and had shed the defensive lean that saw utilities and Treasuries continue to outperform. Investors turned bullish on the notion that the Fed would try to execute a gentle landing on its tapering plans while remaining generally optimistic about earnings growth through the end of the year.

Tapering had been on investors' radars over the past month as multiple Fed governors began to float the idea that the economy had made enough progress to warrant the withdrawal of some level of financial support. Taper tantrum has always been the big fear and there's been a long history of stocks pulling back 10-20% when the Fed has begun attempting to normalize conditions. It seems that its current approach of launching a general taper of asset purchases later this year while keeping interest rates at near zero for another year or more (the December 2022 meeting is the earliest that the Fed futures market is projecting a greater than 50% chance of a rate hike) is striking the right balance of tightening (or less loosening) without running the risk of derailing the recovery.

Is this development worth the strong rally in equities that we saw last week. Sentiment seems to have definitely shifted, but the idea of withdrawing support, even though the degree of such a move is minor, runs counterintuitive to the idea that stock prices should rise. Perhaps investors will reconsider how much they're willing to pay for stocks when interest rates begin rising, but it doesn't appear that is happening in the near future. The launch of tapering had the potential of being the catalyst that sparked a sell-off (keep in mind that the S&P 500 still hasn't seen so much as a 5% decline in stock prices yet in 2021), but that appears to be off the table now.

It's looking more and more like it's going to take some type of shock event in order to spark a sell-off. We've seen stocks correct in the past without a firm "catalyst". For example, the dot-com bubble in 2000 began to burst without a specific event that triggered it (although several events have been blamed in some form or fashion, including Japan slipping into recession, the Fed attempting to raise interest rates or a slowdown in M&A activity stoking viability fears). With the flood of money in the marketplace, there's a level of support and dip buying that have prevented stocks, up to this point, from declining to any significant degree.

The next big risk event could be the debt ceiling debate. 2011 provides a good blueprint for what could happen and October or even September could be the point where the government begins running out of cash and Congress is scrambling to find a solution. I think vigilance is still warranted here, although short-term risks may have subsided.

With that being said, here are three ETFs I'm going to be watching this week and the narratives that go along with them.

Pacer Metaurus U.S. Large Cap Dividend Multiplier 400 ETF (QDPL)

We all know the current state of dividend yields in the financial markets. 30-year Treasuries are earning less than 2%. The S&P 500 is yielding around 1.3%. The pickings are slim among traditional asset classes, but ETF issuers are stepping in to try to fill in the gaps. Pacer already has a unique lineup of funds - free cash flow yielders, targeted REITs, the Trendpilot series - but QDPL adds another interesting twist.

QDPL breaks its exposure down into two components - a price appreciation/depreciation component, through long exposure to the S&P 500, and a dividend income component, consisting of long positions in annual futures contracts that provide exposure to ordinary dividends paid on S&P 500 stocks. The overall exposure to the S&P 500 will be reduced to approximately 88% while the dividend contracts will provide 400% exposure to the dividend component. In other words, you get slightly less upside/downside from the large-cap index in exchange for 4 times the dividend yield. In the current market, that works out to around 5%.

This fund is only a month old, quite small and thinly-traded, so it might not be an ideal investment option just yet, but there are several distinct advantages. The 5% yield is the primary selling point, but so is the fact that it's not being achieved through a covered call strategy. Covered calls limit upside, provide little downside protection and generally only work in sideways, low volatility markets. The dividend contracts provide the outsized yield on top of what works out to be a lower volatility equity portfolio and doesn't necessarily require this sideways, low volatility market in order to succeed.

The 88% S&P 500 exposure might actually be the better way to position a portfolio heading into the last quarter of 2020. The lack of full exposure to the index provides a minor degree of downside protection in a pretty expensive market, while the yield component will certainly appeal to income seekers.

The Pacer Metaurus U.S. Large Cap Dividend Multiplier 300 ETF (TRPL) offers 3 times the yield with 92% of the equity exposure.

Fidelity Stocks For Inflation ETF (FCPI)

Whether it ultimately turns out to be transitory or not remains to be seen, but the current rate of inflation is being watched closely. If it turns out to be temporary, which seems to be the outcome that the market is currently pricing in, risk of a downturn due to this factor specifically seems low. If it doesn't, it could be one of those market surprises that results in an equity correction.

TIPS continue to perform well this year - the SPDR Barclays TIPS ETF (SPIP) has gained 4% this year, while long-term Treasuries have fallen 4% - so there is some degree of inflation protection being added by investors here just in case. While TIPS may be the obvious play for inflation risk, inflation stocks have also worked this year. There are a handful of inflation-related equity ETFs out there. Some are fairly straightforward, some are a bit more complicated. FCPI uses a more complex index methodology but when taken as a whole, it does make sense.

FCPI is "designed to reflect the performance of stocks of large and mid-capitalization U.S. companies with attractive valuations, high quality profiles and positive momentum signals", which is where the "factor" comes into play. From there, it tilts towards industries and sectors that tend to benefit more in an inflationary environment. Specifically, it executes a 5% overweight to energy, materials, consumer staples, healthcare and real assets, while 5% underweighting tech, consumer discretionary, communication services, financials and industrials. The 5% tilts aren't going to significantly alter its differentiation from a broader large-cap index, so this appears to be more of a pure factor portfolio than anything.

Still, FCPI has outperformed the market this year, gaining 24% versus the 21% return of the S&P 500. Given some of the near-term uncertainties from the delta variant, speed of the economic recovery and debt situation, the factor tilts should provide some benefit in minimizing excessive downside risk and pushing too far out on the risk spectrum, while the inflation tilts provide at least a modest risk hedge in case inflation does become more persistent.

Invesco China Technology ETF (CQQQ)

The Chinese tech space has gotten a lot of attention throughout 2021, most recently due to the government's crackdown on internet-heavy businesses, including Alibaba and Tencent. The KraneShares CSI China Internet ETF (KWEB) gets most of the attention here since it's been among the hardest hit. It's still down more than 50% from its highs (although as I noted on Twitter last week, it took in roughly a half billion dollars in a single day, so someone is betting that it's heading back up here).

KWEB, however, isn't a pure tech play. It's got more than 75% of the portfolio in the communication services and consumer discretionary sectors combined. CQQQ is more of your pure tech play and has performed substantially better than KWEB this year based on that fact alone. CQQQ has slightly underperformed the iShares MSCI China ETF (MCHI) year-to-date, but has still done substantially better on a trailing 3-, 5- and 10-year basis.

China and emerging markets in general showed signs of improvement last week, but I'm not convinced the bottom is in. Even if it is, there's a lot of risk involved in taking the chance that this bet would be correct. The country is still imposing lockdown measures, there are still substantial supply chain and shipping issues and the strength of the nation's recovery is in some question. I'd still wait for things to settle down here and conditions to clear up before proceeding.

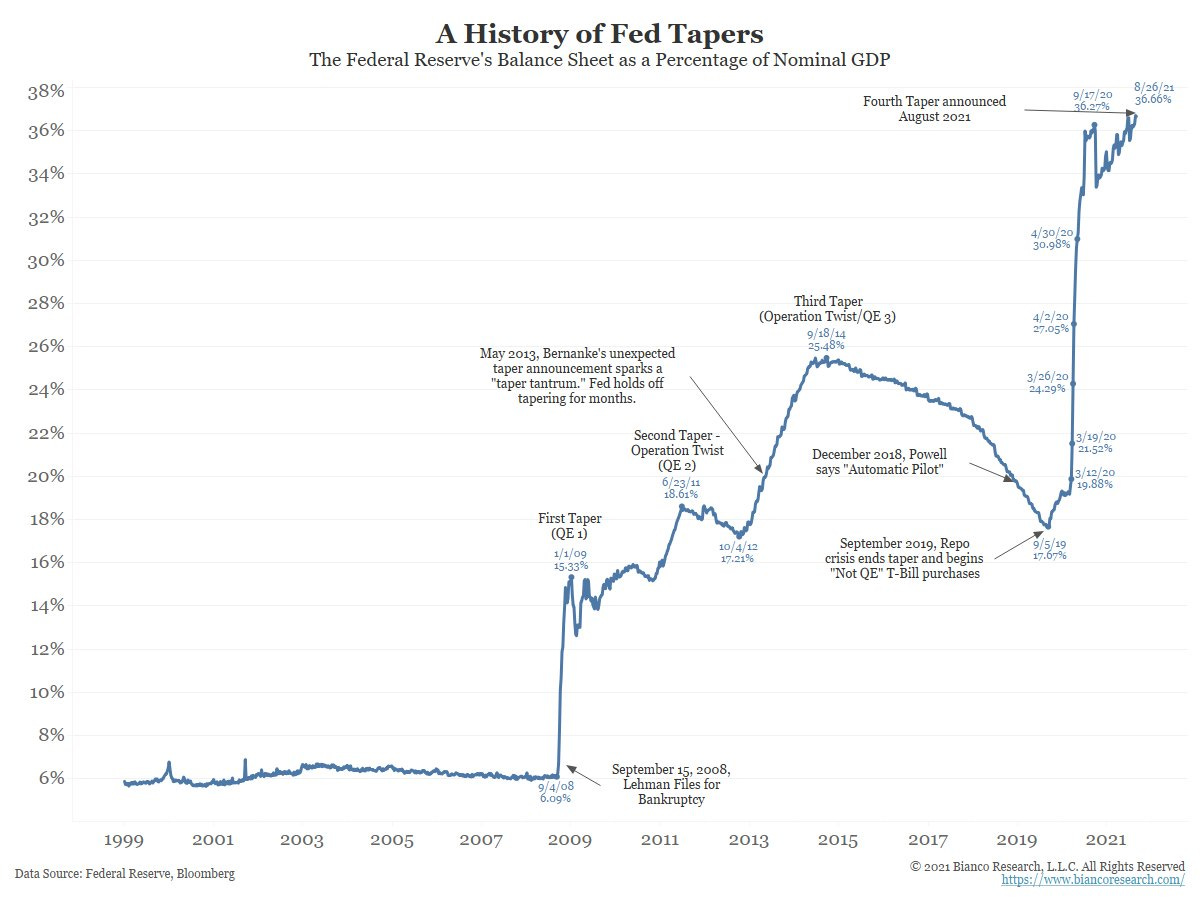

Chart of the Week

The Fed sort of confirmed their plans for tapering bond purchases when Fed Chair Jerome Powell said the central bank was on schedule to begin withdrawing financial support later this year, but stopped short of offering a more specific timeline. The announcement was mostly expected and resulted in equity prices rallying into the tail end of last week instead of falling as is often the case with tapering announcements.

There are a few interesting takeaways from this chart, which details the circumstances of each taper since the financial crisis. The most obvious one is that every instance of tapering over the past 12 years has eventually been met with more tapering. As soon as the Fed begins to try normalizing conditions, something spooks the markets and the central bank steps right back in for support. Sometimes it happens quickly. Sometimes it’s eventual.

The markets reacted favorably to this announcement because it was expected. The majority of the others, especially Bernanke’s 2013 pivot, caught the markets off-guard to some degree and they reacted accordingly. There’s a chance the equity markets handle this taper a little better as long as it’s well telegraphed and slow to progress. I think the Fed has learned from before the risks of unsettling the markets and doesn’t want to do it again.

The other takeaway from this chart is that the Fed always returns. I’m not sure there’s a clear scenario where the Fed brings its balance sheet back down to earth in any major way. It tried in the 2010s and actually made it stick for about 4 years before it swooped in to save the repo market from drying up in late 2019. Then, of course, the COVID pandemic happened and the rules went out the window.

Don’t expect this to be the end for the Fed. If the economy is at risk or the market gets spooked, there’s enough evidence from the past to suggest that the central bank won’t hesitate to make sure asset prices don’t fall too far, too fast. We may no longer live in a world where the global economy is going to be allowed to stand on its own two feet.

Read More…

5 ETFs That Benefited From Bitcoin's Rise To $50,000

American Funds' Parent Finally Gets Into ETFs But Is It Too Late?

The Simple 4 ETF Retirement Portfolio

2 Vanguard ETFs To Power Your Global Dividend Growth

ETF Battles: DVY vs. TLT vs. VNQ - Which Dividend Income ETF Is Better?

Grayscale Plans On Converting GBTC To An ETF; Here's Why That's Not A Good Idea

ETF Battles: CTEC vs. PBW vs. TAN - Which Clean Energy ETF Do You Buy?

Questions, Ideas, Thoughts?

Feel free to reach out by replying to this e-mail or commenting below. Your question or idea might be used in a future newsletter!