Are Long-Term Treasuries About To Become One Of The Best Trades Of 2022?

Yes, this group is 20% off its highs, but here's the case for why it could move sharply higher again.

First of all, yes, I know this isn’t a popular opinion. Long-term Treasuries are nearly 20% off of their recent highs - one of the biggest drawdowns in history. The markets are pricing in as much as 300 basis points more in rate hikes over the next 12 months. Treasury yields look bound to go even higher than they are now. How could I possibly be suggesting that Treasuries may be about to become one of the best trades for the remainder of the year?

Let me make the case.

First of all, I believe the notion that rates will go higher before they go lower. The case for this is that even though economic growth is slowing down, it still doesn’t appear likely that growth will turn negative in 2022. I think that happens at some point in 2023. Because it doesn’t necessarily look like a recession is imminent, it gives investors the opportunity to continue leaning into equities for further potential gains without needing to pivot into safe haven Treasuries just yet. For now, Treasuries can be repriced in accordance to what the Fed plans on doing with interest rates over the next 12 months.

Where do yields top out? The 10-year is at 2.77% as I write this. It seems likely that it’s going to move above 3% before too long. Does it get to 4%? I don’t think so. I think the Fed halts on increasing rates before then and we probably get a dovish pivot as growth slows to the point of turning negative. It feels to me like 3.5% is about as high as it goes.

But I do think recessionary risks are increasing. Although current conditions support the idea of targeting equities for the time being, I think the 2nd half of the year is where things start to pivot. Even if GDP growth rates manage to stay positive this year, here are some of the obstacles the economy is facing:

A Crumbling Housing Market

We’re already seeing those dominoes starting to fall today. Mortgage rates have doubled in just the past several months and are now above 5%. Mortgage applications have already plummeted and we’re seeing evidence that the number of offers per listing is declining. This is likely to only continue as homebuilders began ratcheting up construction of new homes when the housing market was at its peak.

Housing recessions have almost always accompanied broader economic recessions and this one is already starting to take place.

Persistently High Inflation

The market had believed that the current spike in inflation would only be short-term nature and dissipate once supply chains unclogged from the pandemic. Then Russia invaded Ukraine and commodity prices went another leg higher. The conflict is now in its second month with no signs of ending. Now, China has instituted new draconian lockdowns amid the latest COVID outbreak, which threatens to push the country’s economy back into recession and re-clog supply chains. I’d expect high inflation to remain for much longer than expected.

High Energy Prices

This one is probably hurting households the most right now because everybody needs gas for their cars and energy to heat their homes. If Russia remains cut off from the world indefinitely (along with its supplies of crude oil, wheat, corn and other commodities), the high oil and gas prices that are crushing consumer budgets, especially in Europe, are likely here to stay. More money for necessities means less money to spend elsewhere.

Slowing Retail Sales

Speaking of which, U.S. retail sales rose a scant 0.3% in February (March’s number comes later this week, but it’s also expected to be relatively small). This could be one of the bigger indicators that people are starting to spend less as inflation makes everything less expensive. One month doesn’t make a trend, but if we see a similarly small number in March, I think we have to begin thinking that a recession could come sooner than anticipated.

COVID Shutdowns In China

I alluded to this one already up above, but China effectively locking down its economy and its shipping ports is bad for the rest of the world. It raises inflation rates and impacts the ability of companies to produce and sell product. That puts more pressure on the economy to slowdown.

All of this, I believe, is coming. When it does, investors will finally begin rotating out of risk assets and back into Treasuries. I remain skeptical that the Fed will get as far as it wants to with quantitative tightening. The first indication that the Fed is ready to pause, especially if it comes earlier than expected, could be a bullish sign for equities, but I think it would be more important for Treasuries. At that point, the pressure would be off to move rates higher and its status as a safe haven asset could resume.

If the 10-year Treasury yield ends up peaking somewhere in the 3% to 3.5% range, I wouldn’t be surprised to see it pullback about 100 basis points as the slowdown grows closer. The iShares 20+ Year Treasury Bond ETF (TLT) has a duration of around 18 years today. That means we’re looking at an 18% gain if rates were to fall by 1%.

Not a bad deal in today’s market.

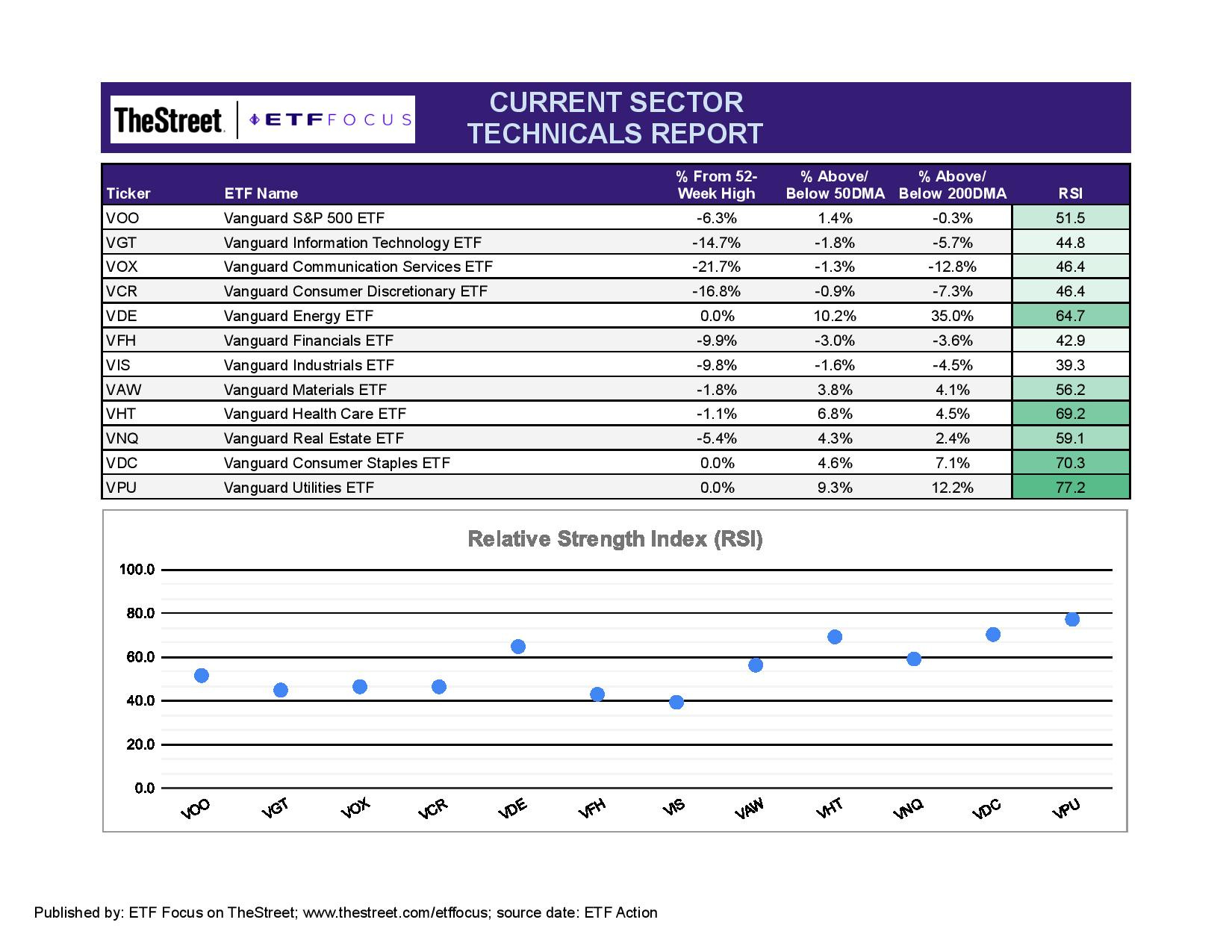

ETF Sector Breakdown

With that being said, let’s look at the markets and some ETFs.

There’s a definite defensive pivot taking place within the U.S. equity market. Over the past two weeks, all of the major defensive sectors - utilities, consumer staples, healthcare and real estate have gained 5%. As Treasuries remain off the table for a lot of investors, conservative stocks, including dividend payers and low volatility stocks, seem to be the alternative. The first three sectors are all effectively in overbought territory, while real estate is on its way. The breadth of this move leads me to believe that there are some legs in this rally.

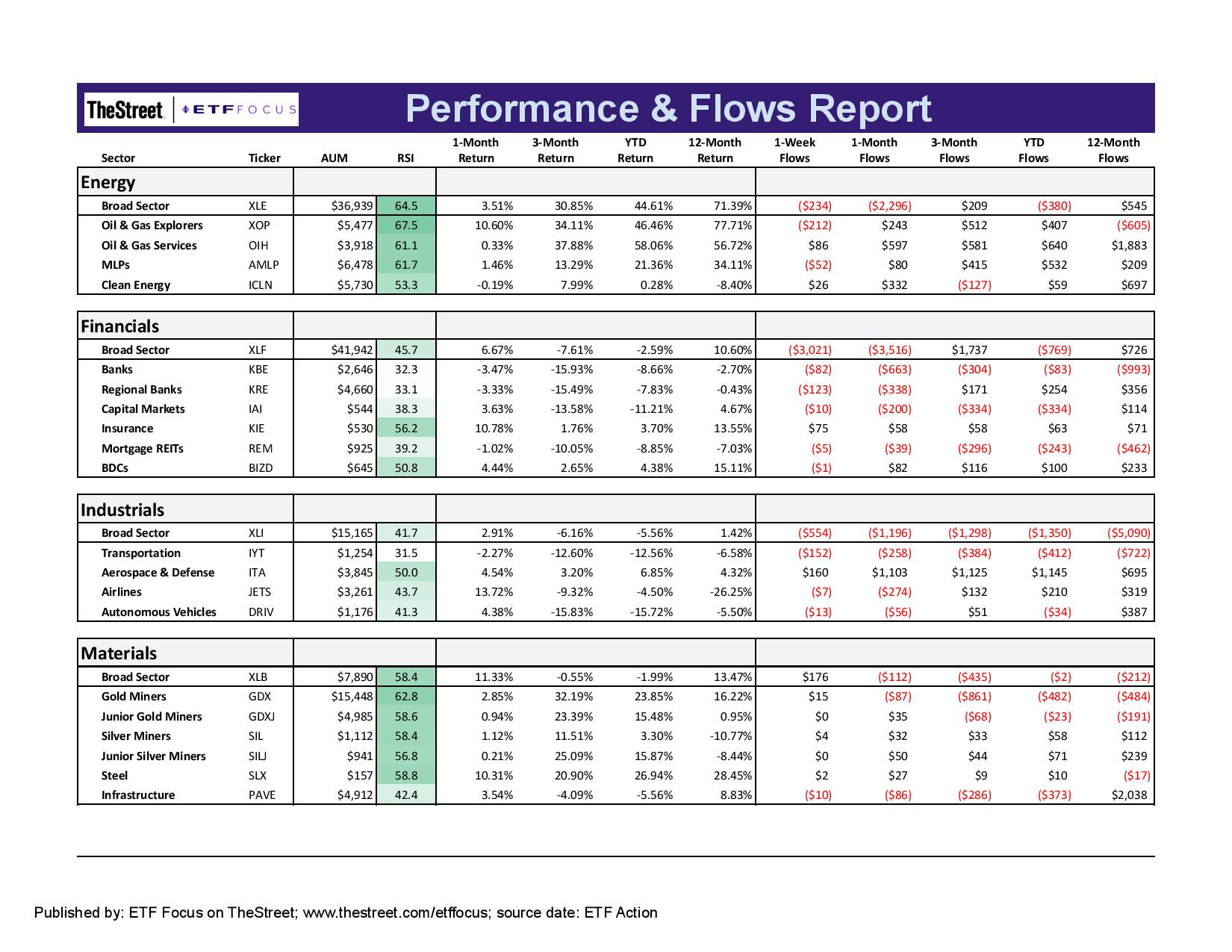

Elsewhere, energy is still looking solid as it has for weeks now. The materials sector is probably the understated outperformer here having lead the market higher thanks to rising commodity prices. Financials and industrials, however, are looking a lot weaker. The latter is going to struggle as input prices get much higher and supply chains look ready to tighten up quite a bit. The housing market will be the biggest risk for the financial sector. If it hasn’t already, lending is about to slow significantly and that’s going to pressure the bottom line.

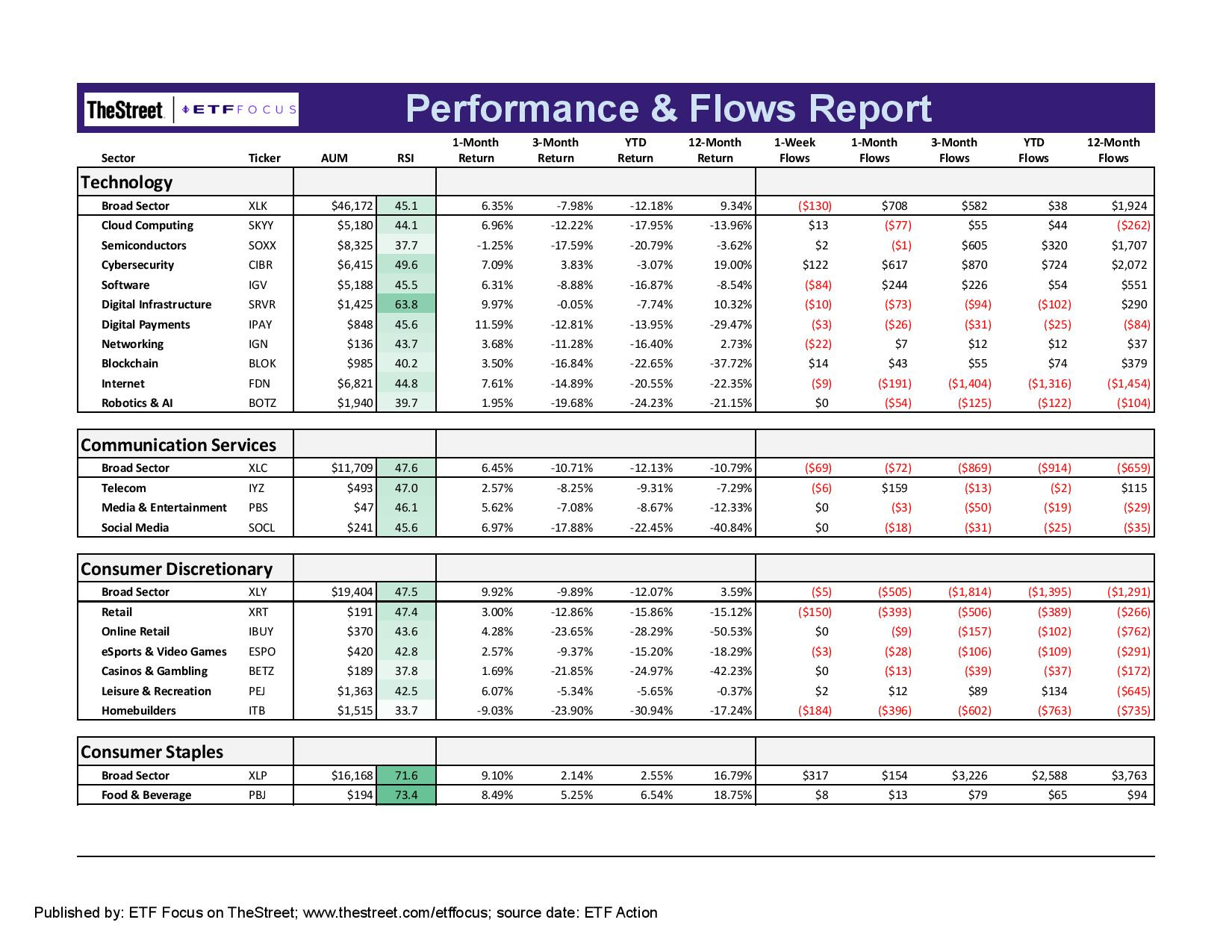

Tech valuations continue to unwind as rates push higher. I don’t this weakness is over either. These stocks are about 15-20% below their recent highs, but that hasn’t been commensurate with the corresponding rise in interest rates. I suspect that these sectors could decline another 10% before all is said and done. The catalysts to make this happen are already in place.

Most of the areas within the three big growth sectors are in relatively neutral territory of not weakening outright, but there are a few outliers. The homebuilders sector is the big one, which I think is in a lot of trouble. Homebuilders have been increasing production (using abnormally expensive lumber at that) when the housing market was peaking, but soaring mortgage rates are about to twist the supply/demand curve in the wrong direction.

Some of the reopening trades are still looking weak. Leisure, hospitality, recreation and gaming stocks are all lagging. Concerns about spending in the face of high inflation are driving this trend. Digital infrastructure is looking good although cybersecurity has moved into neutral territory. Elon Musk’s stake in Twitter failed to ignite a sustainable rally in social media stocks.

The energy sector continues to plow ahead even as crude oil prices begin to moderate here. While explorers are still up about 10% over the past month, servicers, MLPs and clean energy stocks are virtually flat. The sector’s heavyweights - ExxonMobil and Chevron - are also virtually flat here, so this group is no longer the runaway leader in the current market. Volatility has risen and the ups and downs remain fairly sharp, but the continuation of the conflict in Ukraine should add support to keep oil prices high.

Banks have turned into one of the market’s weaker groups and its easy to see why. Rising mortgage rates and a slowdown in the economy are fueling concerns that lending is about to face some massive headwinds. Valuations are still reasonable and there are some dividend income opportunities to be found, but this looks like a sector that’s going to struggle to outperform here. The miners are still looking attractive, but they’re definitely weakening. Silver, especially, has struggled lately, while gold’s quest to the $2000 level looks to have ended for the time being.

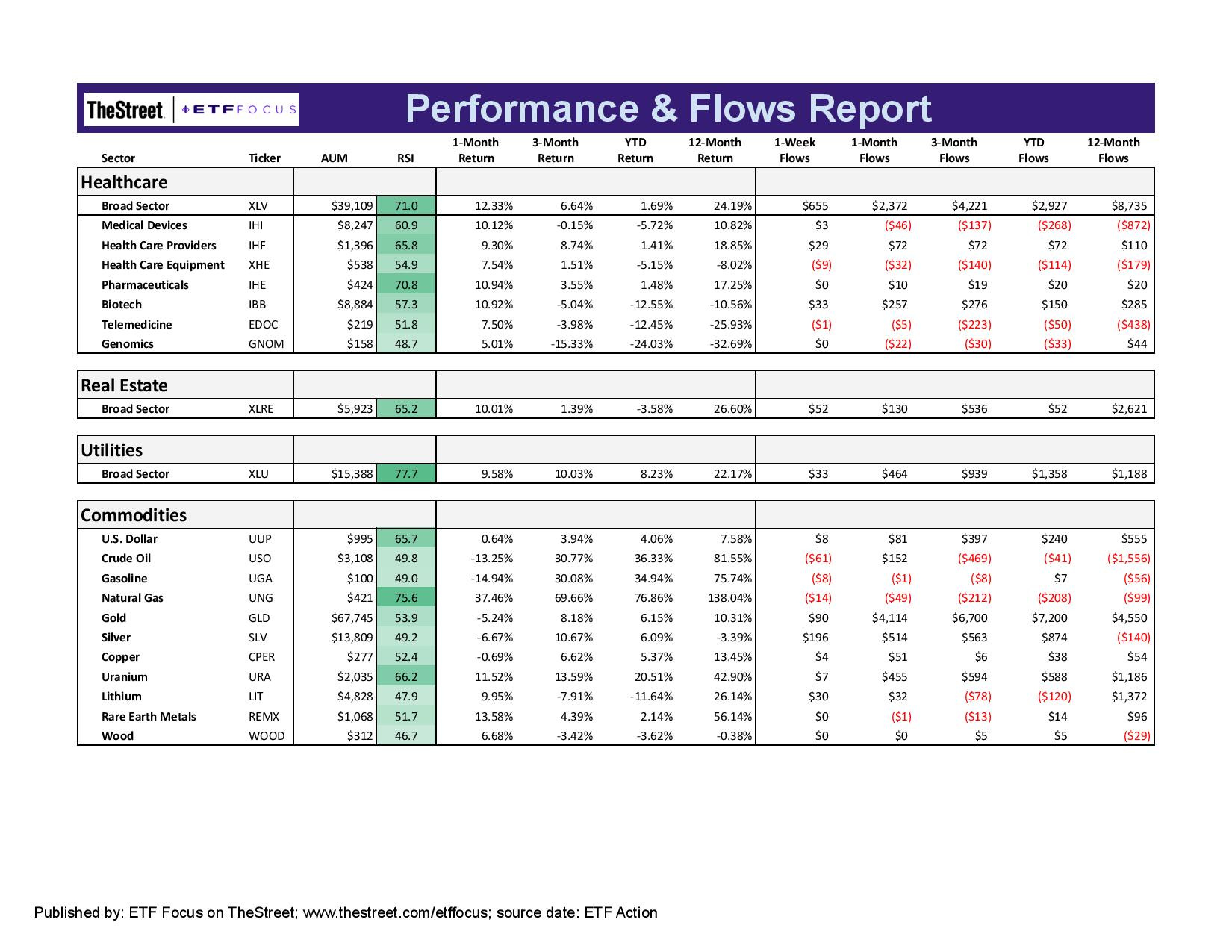

It’s dark green for the defensive sectors almost across the board. Consumer staples and utilities are looking particularly overbought and probably due for a modest breather. Healthcare and real estate aren’t to be ignored either. After struggling for much of 2022, biotech is finally staging a comeback and is one of the best performing subsectors of the past month.

The dollar remains incredibly firm here as it has over the past several months. It recently eclipsed the 100 level thanks to strong gains against both the yen and the euro. Outside of that, natural gas is back in overbought territory after rising nearly 40% in the past month. Lumber continues to weaken, while some of the industrial metals have faded back into neutral territory again.

Read More…

ETF Battles: DEMZ vs. MAGA - Which Politically Driven Stock ETF Is Best?

Recession Watch Is On! 5 ETFs To Protect Your Portfolio Today

Best Performing Dividend ETFs For Q1 2022

Best Performing ETFs For Q1 2022

ETF Battles: ARKK vs. FBCG vs. GK - Which High Growth Stock ETF Is Best?

Using Covered Calls To Turn 2% Yields Into 12% Yields

The Fed Tightening Cycle Is Here, But Will It Work?

ETF Battles: What's The Better High Income Dividend ETF? JEPI vs. NUSI vs. DIVO

Questions, Ideas, Thoughts?

Feel free to reach out by replying to this e-mail or commenting below. Your question or idea might be used in a future newsletter!