5 ETF Storylines For The 2nd Quarter Of 2024

Is the "magnificent 7" trade finished? Can dividend stocks keep their current rally going? What if the Fed doesn't cut rates?

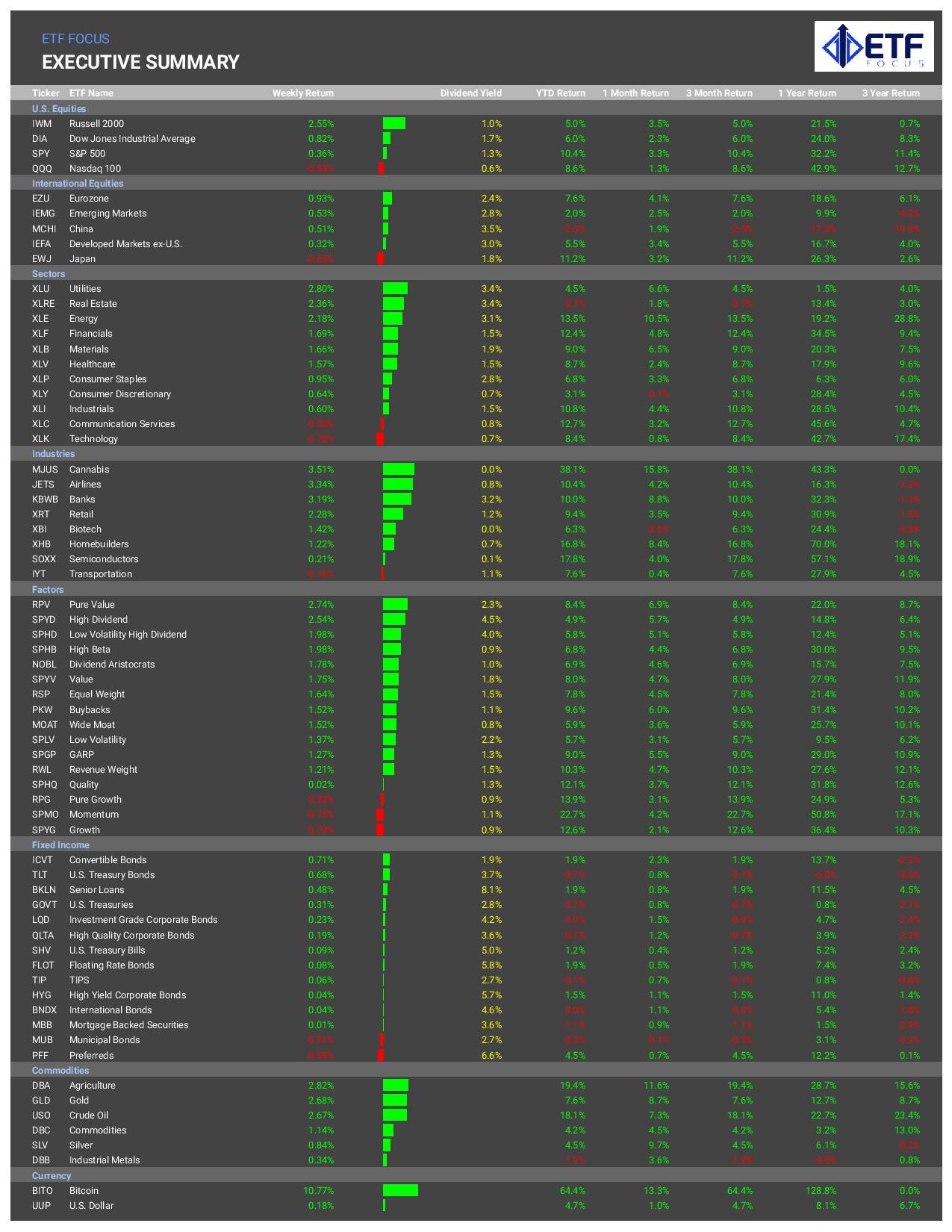

The first quarter of 2024 wrapped up with the S&P 500 adding another 10%, but other indexes, including the Russell 2000 and Nasdaq 100, underperforming. Treasury bonds, which had rallied strongly to close out last year, dipped again in Q1 as investors began unwinding their over-dovish expectations of the Fed's plans.

If there was a theme to the 1st quarter of 2024, it was probably central bank monetary policy decisions.

The Fed entered the year calling for three rate cuts in 2024. Despite an uptick in inflation and improvement in the manufacturing sector, the Fed decided to reiterate its rate cutting plans instead of taking a preemptive hawkish stance. That led to a rotation out of previous leaders, growth and tech, and into cyclicals and value stocks. The story of March has been the re-emergence of the reflation trade, something which could very well carry into April.

On the other side of the ocean, the Bank of Japan made its first rate hike in 17 years, but that was about as far as it went. A very modest 10 basis point increase to its benchmark short-term rate along with no commitment to tighten further anytime in the near future and a continuation of its bond buying program was viewed by the markets as too dovish. Investors grew skeptical of Japan's true economic progress and the yen sold off sharply. Currently, the BoJ stands ready to intervene and defend the yen at any time.

While U.S. large-caps continue to test new all-time highs, the big rally in gold raises questions about whether there is instability building in the currency market. Meanwhile, Iran and Israel may be on the brink of war and the Bank of Israel is already warning of a potential run on the banks.

Clearly, there are some hurdles to overcome as we enter the 2nd quarter of 2024 and a number of storylines to follow.

Here are the five I'll be watching most closely as we approach the summer months.

Can Bitcoin ETF Inflows Maintain Their Current Pace?

The unquestioned biggest development in the ETF space this year has been the launch of spot bitcoin ETFs. Put off by the SEC for about as long as they possibly could have been, these products finally launched officially on January 11th. Nine new ETFs launched that day, while the Grayscale Bitcoin Trust (GBTC) also converted to an ETF.

The reception was huge from the first moment. There wasn't a huge influx of money on day one as some were expecting, but the growth in AUM in these ETFs has been steady and strong since their debut. Total assets in the nine new bitcoin ETFs (we'll set aside GBTC for the time being since it launched with about $28 billion already in hand) have ballooned to a combined $35 billion, about $27 billion of that coming in the form of net new inflows.

The growth in these products has been incredible, but is the pace sustainable? Given the rate of increase so far, the very likely answer is no, but I don't expect these to just stop and stagnate any time soon. There are huge market opportunities still to be tapped that can fuel the next leg of growth.

If financial advisors begin a mass adoption campaign of spot bitcoin ETFs, that could bring potentially thousands of new investors into these funds. If Vanguard ever drops its ban on crypto products (probably unlikely, unfortunately), that's another huge pool of potential new customers.

I'm not going to go out on a limb and try to predict how much is going to be invested in these products by year-end, but I feel comfortable saying it's going to be much more than it is now. BlackRock has unsurprisingly emerged as the early winner in this space, but every one of these products has really been a success. Even WisdomTree's ETF at $75 million in assets is very likely already profitable for the issuer and won't be going anywhere.

Can bitcoin ETF inflows maintain their current pace? Probably not. Are they going to continue to grow? Most definitely!

Does The Fed Signal That Rate Cuts Are Going To Have To Wait?

This is a tougher one to answer and it has big implications for the markets.

If you look purely at the economic numbers, there's no logical reason why the Fed should be considering rate cuts here.

GDP growth is more than 3%

The unemployment rate is below 4%

The 3-month annualized core inflation rate is 4.1%

This isn't the type of backdrop you typically see at the start of rate cutting cycles. With inflation re-accelerating here, you could easily make the argument that a rate hike should be more likely than a rate cut here.

But it doesn't matter what I think the Fed should do. It matters what the Fed will do. And right now there's virtually no one out there that thinks the Fed is considering rate hikes at this point.

Powell just reiterated the Fed's three cut forecast. Even his most hawkish statement recently has only gone as far as saying he wants the inflation data to confirm that it's OK to cut rates. At this point, I think we need to take Powell at his word that the central bank's base case outcome is still three rate cuts in 2024, but I really have a hard time thinking they're going to get there if inflation hangs in the 3-4% range and the U.S. economy keeps churning forward

I know that the Fed probably isn't going to want to rock the boat heading into a presidential election, but I really think that two cuts are more likely than three when all is said and done. The uptick in manufacturing, if it's sustainable, and the move higher in inflation simply don't support three cuts over the next 9 months. I think Powell's messaging might slowly move in that direction heading into or at the June meeting.

Of course, if something falls apart between now and then, all bets are off.

Is The "Magnificent 7" Trade Really Dead?

Market gains really broadened out in March. That was good for cyclicals, value and small-cap stocks, but not so good for previous leaders, especially tech stocks.

Relative to the S&P 500, tech stock outperformance peaked in mid-January, but it's been steady underperformance ever since. The cyclical rotation has resulted in the valuations being squeezed out of more expensive market sectors and that's a trend we could see continue if the Fed remains OK with inflation running above trend.

Does that mean the "magnificent 7" stocks are done? If you look at the group collectively, the answer may appear to be "not yet", but this group is clearly no longer in control the way it once was.

The Roundhill Magnificent 7 ETF (MAGS) is an equal-weight version of these stocks (rebalanced quarterly). This chart suggests that the group is still holding its own relative to the S&P 500 even though it's simply keeping pace with the index now.

Within the group of 7, however, has been chaos. NVIDIA is by far the best performer year-to-date, currently up more than 80%, but Facebook has also gained an impressive 40%. On the other end of the spectrum, Tesla is down more than 30%, while Apple is down 12%. Whereas every member of the group was delivering market-destroying returns last year, it's just individual success stories now.

The thing is that these companies have delivered strong growth over the past 12-24 months and deserve at least a good chunk of the gains they've posted, but peak enthusiasm appears to have passed. In this type of reflationary environment, expect growth stocks to see their valuations trimmed somewhat. If we go back to the high growth, low inflation environment it looked like we were moving into previously, the magnificent 7 could find new life again. In Q2, however, it might be tough sledding.

Can Dividend Stocks Keep Up Their Recent Outperformance?

Here's something that income seekers will appreciate! Dividend stocks have actually begun outperforming the S&P 500 again!

It's been a relatively short renaissance, to be fair, but it's been the best run this group has had since at least the 4th quarter of last year and maybe even going back to the end of 2022.

Dividend stocks often get the reputation of being defensive stocks, but that's an inaccurate representation. Sure, there are utilities and consumer staples stocks in there, but they're also typically overweight in financials and industrials (and maybe energy stocks depending on the individual strategy). So they've clearly benefited from the most recent cyclical rally as much as anybody and that's what's driven outperformance over the past couple months.

As long as tech & growth doesn't dominate the equity markets in the way they did during most of 2023, dividend stocks have a fighting chance of doing well against the S&P 500. 2022, for example, was a great example of a traditional risk-off market and dividend stocks beat the S&P 500 by double digits. In the current reflationary cycle where financials, industrials and energy are leading, dividend stocks are still outperforming.

Given that growth is underperforming and the Fed's narrative makes it more likely than not that it will stay that way, I think there's a clear path for dividend stocks and ETFs to continue doing well. High yielders have done better than more conservative dividend growth strategies over the past month or two suggesting that investors are still comfortable taking risks here. If that trend remains intact, I think this rally has legs.

Does The Weak Japanese Yen Risk A Global Market Volatility Spike?

The Bank of Japan's first rate hike in 17 years was supposed to improve investor perception that the nation's economy was on the right track. It was supposed to strengthen the yen.

Instead, it's more of the same. The BoJ's inability to commit to further tightening measures portrayed weakness instead of strength and the yen is back to hovering near 30-year lows relative to the dollar.

That's not necessarily a bad thing for some traders who have long relied on the yen carry trade to improve their interest rate differentials (the carry trade involves borrowing cheap yen in order to invest in securities with much higher interest rates, such as U.S. Treasuries). A weak yen is a good thing for them, but what happens if that falls apart?

The Bank of Japan has already said that it's standing ready to buy yen in order to increase its value. That would certainly make the yen more volatile and potentially damage the yen carry trade for a number of traders. That's one way to effectively tighten policy without raising interest rates. But that's a manual intervention not based on the economic winds. What happens if investors keep dumping yen and making it weaker still? Will the BoJ be forced to raise interest rates to make Japanese currency and fixed income products more attractive?

Once you get into a series of steps like this, the whole system becomes more volatile and less stable. More volatility, of course, tends to correlate highly with market sell-offs. The next month or two could go a long way in determining how the rest of the year will go.

Final Thoughts

Even though there are some risks brewing, I think the market is set up pretty well for the next couple months. The Fed looks like it's willing to keep supporting growth here and the latest economic numbers & labor market data look supportive as well.

I'm concerned about the trajectory of inflation and the risks posed by what's happening in China and Japan. Inflation could very well look contained for at least the next quarter, but Asia could pop at any time pretty unexpectedly.

Thanks for reading!